ACCA F3重难点解析9个case帮你理清F3重难点.docx

ACCA F3重难点解析9个case帮你理清F3重难点.docx

- 文档编号:9978993

- 上传时间:2023-02-07

- 格式:DOCX

- 页数:10

- 大小:50.44KB

ACCA F3重难点解析9个case帮你理清F3重难点.docx

《ACCA F3重难点解析9个case帮你理清F3重难点.docx》由会员分享,可在线阅读,更多相关《ACCA F3重难点解析9个case帮你理清F3重难点.docx(10页珍藏版)》请在冰豆网上搜索。

ACCAF3重难点解析9个case帮你理清F3重难点

ACCAF3重难点解析——9个case帮你理清F3重难点!

自从F3实行机考后,考前猜题变得毫无意义。

楷博财经现将教学过程中,同学们遇到的部分重难点做出解析。

Case1

Erinisregisteredforsalestax.DuringMay,shesellsgoodswithataxexclusivepriceof$600toKyleoncredit.AsKyleisbuyingalargequantityofgoods,Erinreducesthepriceby5%.Shealsooffersadiscountofanother3%ifKylepayswithin10days.Kyledoesnotpaywithinthe10days.Ifsalestaxischargedat17.5%,whatamountshouldErinchargeonthistransaction?

解析

信用交易发生的时点,卖方要开具销售发票,此时会有一个假设:

买方会在10天内支付货款,从而得到earlydiscount(3%)

因此,此交易产生的销项税为$600X95%X97%X17.5%

如果买方在10天后才支付,需要补开一张发票,票面销项税为$600X95%X3%X17.5%

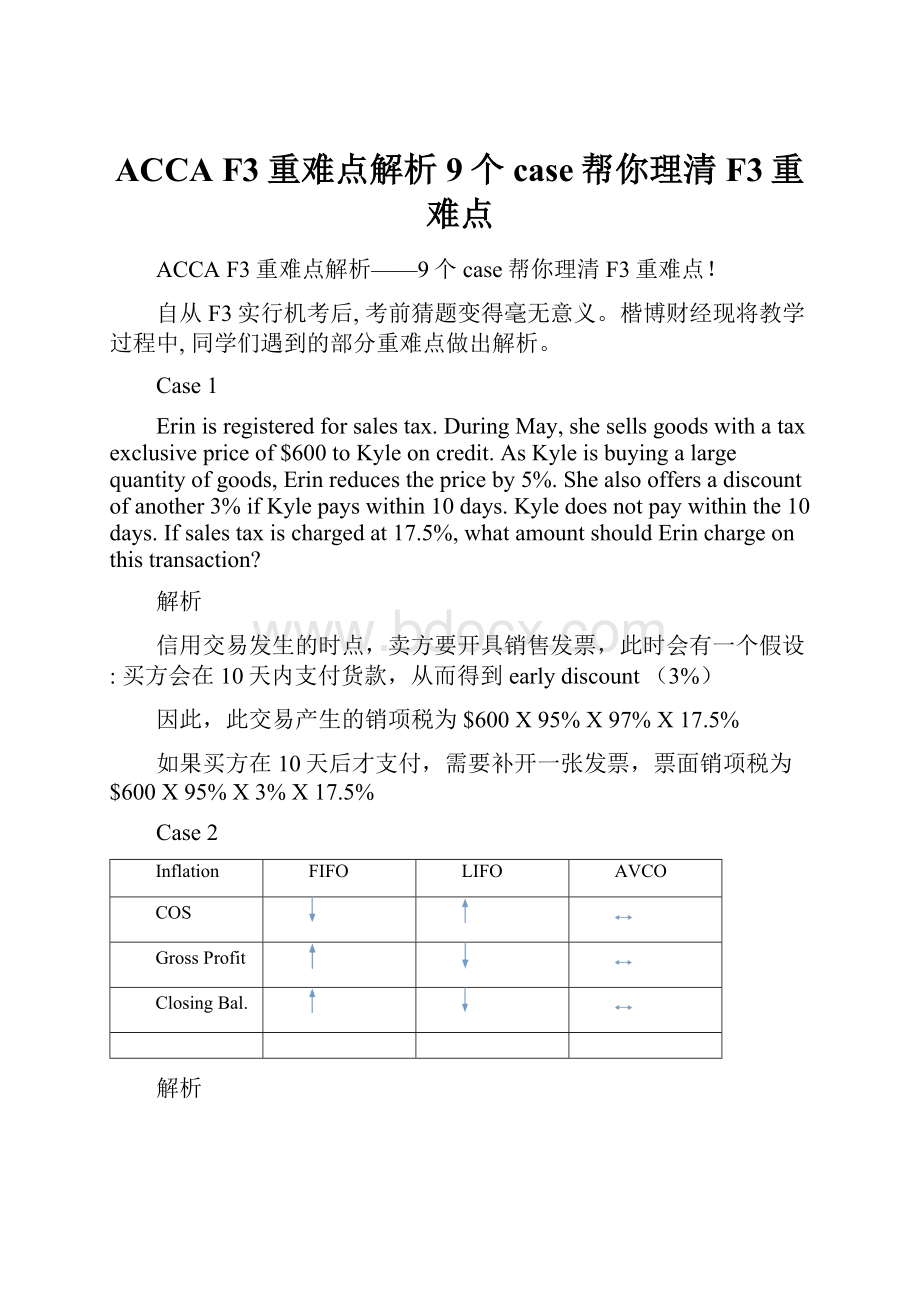

Case2

Inflation

FIFO

LIFO

AVCO

COS

GrossProfit

ClosingBal.

解析

在采购价格一直上涨的背景下(i.e.inflation),公司使用3种Valuationmethods,对Costofsales,profitandclosinginventoryvalue的影响总结如上.英文表述如下:

Duringinflationaryperiod,FIFOgivesthehighestclosingvalueandprofit,butlowestCOS;

Duringinflationaryperiod,LIFOgivesthelowestclosingvalueandprofit,buthighestCOS;

AVCOalwaysstandinthemiddle.

Case3

Chapter6Inventory中2个"特殊"会计分录

(1)Owner拿公司存货自用

Dr.Equity(所有者权益减少)

Cr.Inventorydrawing(orPurchaseorCOS)(COS减少)

(2)拿公司存货作为固定资产使用,如电脑

Dr.Non-currentasset(固定资产增加)

Cr.COS(orPurchase)(期间采购成本减少或COS减少)

解析

国际会计准则下,公司对期间存货增加或减少不会记录在会计系统中的Ledgeraccount(i.e.Inventoryledgeraccount),即如下会计分录是错误的:

Dr.Inventory

Cr.Payablesorcash

我们将期间采购(赊购或现金采购)行为视为"采购费用"的发生,即:

Dr.Purchase

Cr.Payablesorcash

也就是说,期间存货减少,我们不能贷记Inventory.

Case4

Chapter10的年末调整分录,对P&LandB/S的影响如下:

应计费用

预付费用

应计收入

预收收入

Accrual

Prepayment

Accruedincome

PrepaidIncome

Accounting

Entries

Dr费用

Cr应计费用

Dr预付费用

Cr费用

Dr应计收入

Cr收入

Dr收入

Cr预收收入

P&L:

B/S:

费用利润

费用利润

收入利润

收入利润

流动负债

流动资产

流动资产

流动负债

Case5

Chapter11

On1January2013Tipton’stradereceivableswere$10,000.Thefollowingrelatestotheyearended31December2013:

Creditsales$100,000

Cashreceipts$90,000

Discountsallowed$800

Discountsreceived$700

Cashreceiptsinclude$1,000inrespectofareceivablepreviouslywrittenoff.Calculatetheclosingvalueofreceivable:

解析

Method1:

Theclosingbalance=Opening+Addition–Receipts–Discount+baddebtsrecovered

=10,000+100,000–90,000–800+1,000

Note:

DiscountreceivedhasnothingtodowithsalesorTR

Method2:

Note1:

期间从信用客户收到$90,000其中$1,000之前已经作为坏账writeoff,现在收到了这笔钱,不能视为Receivable的减少.参见下面的分录:

Before1

1.Cashreceived

DrIrrecoverabledebts1,000

DrBank1,000

CrTR1,000

CrIrrecoverabledebts1,000

Method3:

之前将之writeoff

随后客户通知准备还钱

真正收到钱

DrIrrecoverabledebts1,000

DrTR1,000

DrBank1,000

CrTR1,000

CrIrrecoverabledebts1,000

CrTR1,000

Note:

Method2and3的区别在于:

method2没有做中间的分录

Case6

Chapter12Provisionandcontingentliability

IAS37requirescontingentliabilitiesandassetsaresummarizedinthefollowingtable:

ProbabilityofOccurrence

Liabilities

Assets

Virtuallycertain(>95%)

Recognize

(确认为负债如TP)

Recognize

(确认为资产如TR)

Probable(51%-95%)

Provideanddiscloseinnote

Discloseinnote

Possible=notlikely(5%-50%)

Discloseinnote

Ignore

Remote(<5%)

Ignore

Ignore

Case7

Chapter13Capitalstructure

Approvingbody

Accountingentries

Mid-year/

interimdividend

Boardofdirectors

DrRetainedEarnings-Dividends

CrBank(B/S)

Finaldividend

AnnualGeneralMeeting(AGM)

DrRetainedEarnings-Dividends

CrDividendspayable(B/S)

12.301.1

ApprovedYEApproved

FinaldeclareddividendFinalproposeddividend

DrRE-DividendsNoaccountingentries

CrDividendspayableDiscloseinNotes

解析

年末对普通股股东分红,需得到股东大会的批准.得到批准的时点很重要,如果是年末前得到Approval,则叫做Finaldeclareddividend;年后得到Approval,则Finalproposeddividend.对于2种情况的会计处理如上。

Case8

Chapter13Capitalstructure

Corporationtax

Over-provision

Under-provision

2015.12.31Estimatetaxfor2015

1DrTaxCharge$1,000

CrTaxpayable$1,000

对2015年应纳税金作出预估

2015.12.31Estimatetaxfor2015

1DrTaxCharge$1,000

CrTaxpayable$1,000

对2015年应纳税金作出预估

2016.2.2Taxmancollectsthetax

2DrTaxPayable$800

CrBank$800

源于年末多提,实际比预估少200(Over-provision)

导致TaxPayable贷方余额200

2016.2.2Taxmancollectsthetax

2DrTaxPayable$1,200

CrBank$1,200

源于年末少提,实际比预估多200(Under-provision)

导致TaxPayable借方余额200

2016.12.31本期已经付清属于去年的税金,因此对TaxPayable科目贷方余额调整:

YEAdjustment

3DrTaxpayable$200

CrTaxcharge$200

后果:

导致2016年计入P&L的taxcharge______

导致2016年taxpayable余额=________

2016.12.31本期已经付清属于去年的税金,因此对TaxPayable科目借方余额作出调整:

YEAdjustment

3DrTaxcharge$200

CrTaxpayable$200

导致2016年计入P&L的taxcharge_______

导致2016年taxpayable余额=________

1+2+3=

DrTaxcharge$800

CrBank$800

1+2+3=

DrTaxcharge$1,200

CrBank$1,200

解析

上述故事,源自公司去年年末对去年税费预提时,出现了多提或少提的情况.

因此我们在本年年末,做出3的调整分录.

Case9

Chapter17Preparingfinancialstatement

Typesofadjustment

Doubleentry

Impact

Chapter

Openinginventory

DrCostofsales

CrInventory

P&L

B/S

6

Closinginventory

DrInventory

CrCostofsales

B/S

P&L

6

Depreciationchargefortheyear

DrDepreciationexpense

CrAccumulateddepreciation

P&L

B/S

7

Accrualsandprepayment

参见Case4

10

Irrecoverabledebts

DrIrrecoverableexpense

CrReceivables

P&L

B/S

11

Allowanceforreceivables

Increaseinallowance:

DrIrrecoverabledebt

CrAllowanceforreceivable

Decreaseinallowance:

DrAllowanceforreceivable

CrIrrecoverabledebtexpense

P&L

B/S

B/S

P&L

11

Taxestimatefortheyear

DrTaxcharge

CrCurrenttaxliabilities

P&L

B/S

13

Adjustmentsforprioryear'staxestimates

Over-provisioninprioryear:

DrCurrenttaxprovision

CrTaxchargeforthisyear

Under-provisioninprioryear:

DrTaxchargeforthisyear

CrCurrenttaxprovision

B/S

P&L

P&L

B/S

(图10)

解析

在17章编制财务报表过程中,有很多年末调整事项.以上总结了这些调整事项.注意每个调整分录,影响的是2个不同的主表:

P&LorBalancesheet.

以上就是楷博财经对F3的9个经典题型的解析,希望同学们在考试中,能够举一反三,最后能在考试中取得优异的成绩。

- 配套讲稿:

如PPT文件的首页显示word图标,表示该PPT已包含配套word讲稿。双击word图标可打开word文档。

- 特殊限制:

部分文档作品中含有的国旗、国徽等图片,仅作为作品整体效果示例展示,禁止商用。设计者仅对作品中独创性部分享有著作权。

- 关 键 词:

- ACCA F3重难点解析9个case帮你理清F3重难点 F3 难点 解析 case 理清

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

《城市规划基本知识》深刻复习要点.docx

《城市规划基本知识》深刻复习要点.docx

-

《高电压技术》word版.docx

-

《安全带》gb6095.docx

-

BCP计划应急计划.docx

-

《计算机组成与工作原理》第一章复习题.docx

-

CANON LBP系列激光打印机使用方法指南.docx

-

C语言课程设计火车票系统源代码.docx

-

3热力管道沟槽开挖方法.docx

-

HR岗位职责.docx

-

1 脱硫脱硝cems维护技术规范.docx

-

O2O超市商业项目计划书.docx

-

SCI期刊呼吸胸外.docx

-

18岁生日祝福语短信.docx

-

ITMC物流企业经营沙盘比赛规则.docx

-

XX钢绳成本管理.docx

-

Matlab的第三方工具箱大全强烈推荐.docx

-

安全保卫工作先进个人.docx

-

安全生产工作日记.docx

-

windows 漏洞集合.docx

-

Φ160数控落地镗铣床技术规格.docx

-

安全施工组织设计.docx

-

安全检查和隐患排查治理制度及记录.docx

-

部编版小学二年级语文下册课外阅读专项.docx

-

变电站投运前质量监督检查汇报材料模版.docx

-

版 创新设计 高考总复习 历史 北师大版第一部分 必考内容第十五单元 第38讲.docx

-

本科毕业设计论文.docx

-

北京大学社会心理学串讲笔记1一10章加试题.docx

-

亳州市教坛新星骨干教师学科带头人特级教师年度考核细则知识分享.docx

-

超星尔雅《人生与人心》期末考试满分答案.docx

-

财经法规与会计职业道德案例分析题.docx

-

茶文化会发言稿.docx

-

财务会计核算实习总结.docx

-

侧卸式装岩机司机安全操作规程通用范本Word文档格式.docx

-

常见电压比较器分析比较Word文档格式.docx

-

读《西游记》有感集合10篇Word下载.docx

-

伯克利下肢外骨骼BLEEX的机械学设计Word格式.docx

-

symbianUII文档格式.docx

-

程序设计艺术与方法课程实验报告Word文档格式.docx

-

给客户的端午节快乐经典问候语Word下载.docx

-

层序地层总结Word文档下载推荐.docx

-

度安全培训计划Word下载.docx

-

北京市昌平区届高三第二次统一练习理综物理试题docWord文件下载.docx

-

步进电机可编程驱动控制器设计资料及例程文档格式.docx

-

常用材料之间的摩擦系数全Word格式.docx

-

财政突发公共事件应急方案Word文档格式.docx

-

给情人的早安短信Word下载.docx

-

材料力学习题册Word下载.docx

-

度优秀博物馆实习报告模板五篇Word文档格式.docx

-

采矿生产实习岗位工作总结Word文档下载推荐.docx

-

pcb实习心得.docx

-

HSE管理体系.docx