最新中级财务会计英文版课后答案chap06.docx

最新中级财务会计英文版课后答案chap06.docx

- 文档编号:809411

- 上传时间:2022-10-13

- 格式:DOCX

- 页数:11

- 大小:22.59KB

最新中级财务会计英文版课后答案chap06.docx

《最新中级财务会计英文版课后答案chap06.docx》由会员分享,可在线阅读,更多相关《最新中级财务会计英文版课后答案chap06.docx(11页珍藏版)》请在冰豆网上搜索。

最新中级财务会计英文版课后答案chap06

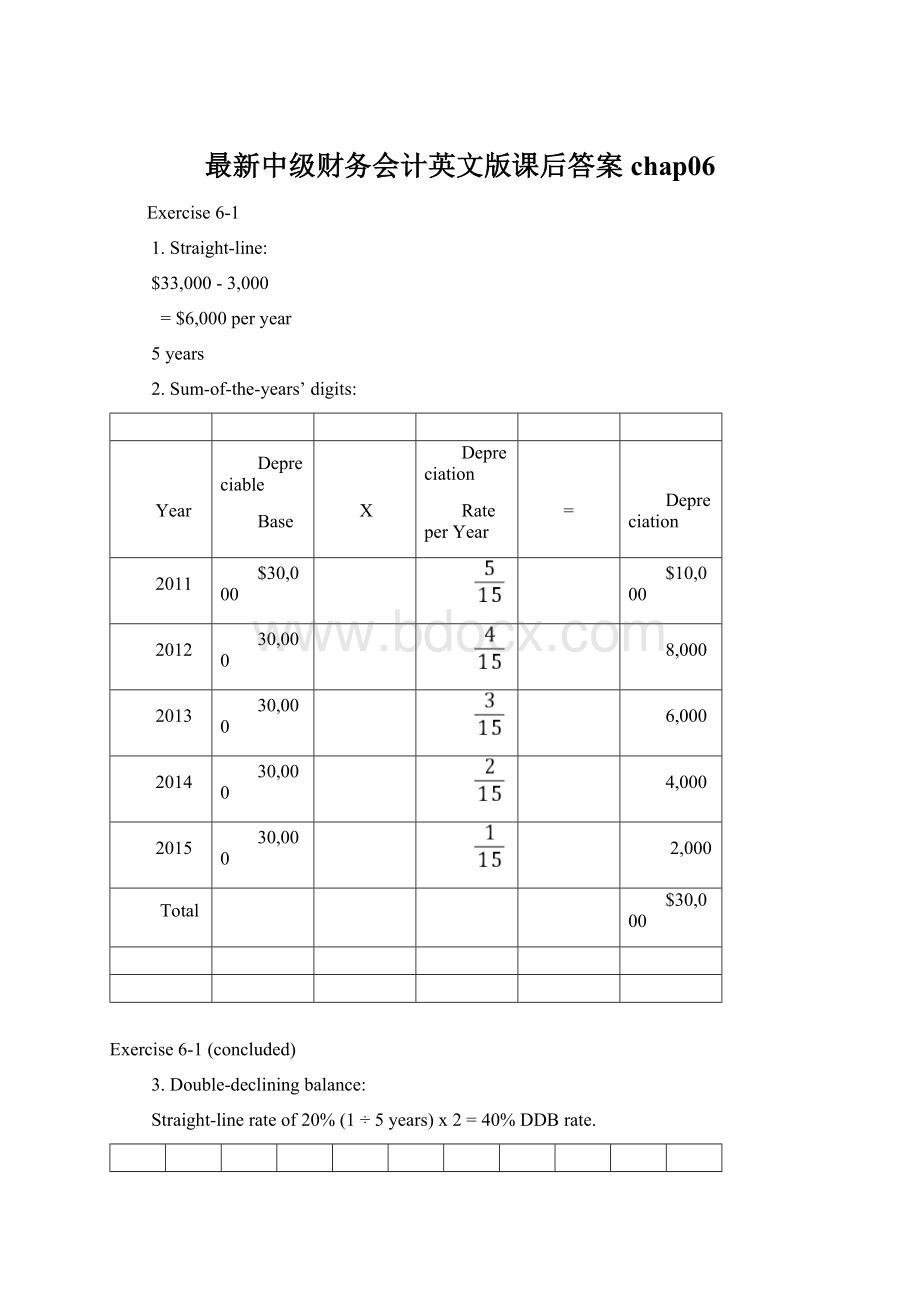

Exercise6-1

1.Straight-line:

$33,000-3,000

=$6,000peryear

5years

2.Sum-of-the-years’digits:

Year

Depreciable

Base

X

Depreciation

RateperYear

=

Depreciation

2011

$30,000

$10,000

2012

30,000

8,000

2013

30,000

6,000

2014

30,000

4,000

2015

30,000

2,000

Total

$30,000

Exercise6-1(concluded)

3.Double-decliningbalance:

Straight-linerateof20%(1÷5years)x2=40%DDBrate.

Year

BookValueBeginning

ofYearX

Depreciation

Rateper

Year=

Depreciation

BookValue

EndofYear

2011

$33,000

40%

$13,200

$19,800

2012

19,800

40%

7,920

11,880

2013

11,880

40%

4,752

7,128

2014

7,128

40%

2,851

4,277

2015

4,277

*

1,277*

3,000

Total

$30,000

*Amountnecessarytoreducebookvaluetoresidualvalue

4.Units-of-production:

$33,000-3,000

=$.30permiledepreciationrate

100,000miles

Year

Actual

Miles

DrivenX

Depreciation

Rateper

Mile=

Depreciation

BookValue

Endof

Year

2011

22,000

$.30

$6,600

$26,400

2012

24,000

.30

7,200

19,200

2013

15,000

.30

4,500

14,700

2014

20,000

.30

6,000

8,700

2015

21,000

*

5,700*

3,000

Totals

102,000

$30,000

*Amountnecessarytoreducebookvaluetoresidualvalue

Exercise6-2

1.Straight-line:

$115,000-5,000

=$11,000peryear

10years

2.Sum-of-the-years’digits:

Sum-of-the-digitsis([10(10+1)]÷2)=55

2011$110,000x10/55=$20,000

2012$110,000x9/55=$18,000

3.Double-decliningbalance:

Straight-linerateis10%(1÷10years)x2=20%DDBrate

2011$115,000x20%=$23,000

2012($115,000-23,000)x20%=$18,400

4.Onehundredfiftypercentdecliningbalance:

Straight-linerateis10%(1÷10years)x1.5=15%rate

2011$115,000x15%=$17,250

2012($115,000-17,250)x15%=$14,663

5.Units-of-production:

$115,000-5,000

=$.50perunitdepreciationrate

220,000units

201130,000unitsx$.50=$15,000

201225,000unitsx$.50=$12,500

Exercise6-3

1.Straight-line:

$115,000-5,000

=$11,000peryear

10years

2011$11,000x3/12=$2,750

2012$11,000x12/12=$11,000

2.Sum-of-the-years’digits:

Sum-of-the-digitsis{[10(10+1)]/2}=55

2011$110,000x10/55x3/12=$5,000

2012$110,000x10/55x9/12=$15,000

+$110,000x9/55x3/12=4,500

$19,500

3.Double-decliningbalance:

Straight-linerateis10%(1÷10years)x2=20%DDBrate

2011$115,000x20%x3/12=$5,750

2012$115,000x20%x9/12=$17,250

+($115,000-23,000)x20%x3/12=4,600

$21,850

or,

2012($115,000-5,750)x20%=$21,850

4.Onehundredfiftypercentdecliningbalance:

Straight-linerateis10%(1÷10years)x1.5=15%rate

2011$115,000x15%x3/12=$4,313

2012$115,000x15%x9/12=$12,937

+($115,000-17,250)x15%x3/12=3,666

$16,603

Or,

2012($115,000-4,313)x15%=$16,603

Exercise6-3(concluded)

5.Units-of-production:

$115,000-5,000

=$.50perunitdepreciationrate

220,000units

201110,000unitsx$.50=$5,000

201225,000unitsx$.50=$12,500

Exercise6-4

Buildingdepreciation:

$5,000,000-200,000

=$160,000peryear

根本不知道□30years

二、资料网址:

Buildingadditiondepreciation:

Beadwrks公司还组织各国的“芝自制饰品店”定期进行作品交流,体现东方女性聪慧的作品曾在其他国家大受欢迎;同样,自各国作品也曾无数次启发过中国姑娘们的灵感,这里更是创作的源泉。

图1-1大学生月生活费分布RemainingusefullifefromJune30,2011is27.5years.

附件

(二):

7、你喜欢哪一类型的DIY手工艺制品?

$1,650,000

(4)牌子响=$60,000peryear

27.5years

2011$60,000x6/12=$30,000

我们从小学、中学到大学,学的知识总是限制在一定范围内,缺乏在商业统计、会计,理财税收等方面的知识;也无法把自己的创意准确而清晰地表达出来,缺少个性化的信息传递。

对目标市场和竞争对手情况缺乏了解,分析时采用的数据经不起推敲,没有说服力等。

这些都反映出我们大学生创业知识的缺乏;2012$60,000x12/12=$60,000

为此,装潢美观,亮丽,富有个性化的店面环境,能引起消费者的注意,从而刺激顾客的消费欲望。

这些问题在今后经营中我们将慎重考虑的。

Exercise6-6

Requirement1

(二)创业优势分析

1.Straight-line:

$260,000-20,000

=$40,000peryear

6years

2011$40,000x8/12=$26,667

2012$40,000x12/12=$40,000

2.Sum-of-the-years’digits:

Sum-of-the-years’digitsis([6(6+1)]÷2)=21

2011$240,000x6/21x8/12=$45,714

2012$240,000x6/21x4/12=$22,857

+$240,000x5/21x8/12=38,095

$60,952

3.Double-decliningbalance:

1/6(thestraight-linerate)x2=1/3DDBrate

2011$260,000x1/3x8/12=$57,778

2012$260,000x1/3x4/12=$28,889

+($260,000–86,667)x1/3x8/12=38,518

$67,407

or,

2012($260,000–57,778)x1/3=$67,407

Exercise

- 配套讲稿:

如PPT文件的首页显示word图标,表示该PPT已包含配套word讲稿。双击word图标可打开word文档。

- 特殊限制:

部分文档作品中含有的国旗、国徽等图片,仅作为作品整体效果示例展示,禁止商用。设计者仅对作品中独创性部分享有著作权。

- 关 键 词:

- 最新 中级 财务会计 英文 课后 答案 chap06

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

12处方点评管理规范实施细则_精品文档.doc

12处方点评管理规范实施细则_精品文档.doc

-

12核心制度竞赛题库_精品文档.doc

-

12新医疗技术准入制度_精品文档.docx

-

12月份医务科质控通报_精品文档.doc

-

12项基本公共卫生服务项目_精品文档.docx

-

12月环境卫生学监测方法考核试题_精品文档.doc

-

13双重预防体系风险评价制度及准则_精品文档.doc

-

12种不能忽视的可能的心脏病症状_精品文档.doc

-

13检验科“三基”考试试卷_精品文档.doc

-

14以预防为先导_精品文档.doc

-

12高危药品分级管理制度及目录_精品文档.doc

-

13个病种中医护理方案_精品文档.docx

-

16检验科应对突发事件应急预案_精品文档.docx

-

12急救药品管理制度_精品文档.doc

17种抗癌药纳入国家基本医疗保险工伤保险和生育保险药品目录_精品文档.xls

17种抗癌药纳入国家基本医疗保险工伤保险和生育保险药品目录_精品文档.xls

-

14医疗器械召回程序_精品文档.wps

-

13医用耗材库房管理制度_精品文档.doc

-

136个幼儿园英语课堂游戏_精品文档.docx

-

12经络彩图_精品文档.doc

-

151颅脑损伤恢复期康复临床路径_精品文档.doc

-

14项护理核心制度_精品文档.doc

-

12检验科化学危险物品使用准则_精品文档.doc

-

15-消化内镜手术分级目录_精品文档.xls

-

13术前讨论记录本模板_精品文档.doc

-

17-下腰痛评估表JOAVAPS_精品文档.doc

-

12项基本公共卫生服务流程图_精品文档.doc

-

13中国髋膝关节置换的现状及展望_精品文档.docx

-

14种最迷惑人的癌症前兆_精品文档.docx

-

17消毒供应室医院感染管理制度_精品文档.doc

-

15附加住院津贴保险条款的费率-人保财险备-健康附号_精品文档.doc

-

19陕西省崔家沟监狱罪犯医疗防疫总站突发事件预案_精品文档.doc

-

20项护理技术操作规程及评分标准_精品文档.doc

-

初中毕业典礼演讲稿演讲稿Word文档下载推荐.docx

-

浅析35KV线路接地电阻与防雷标准版文档格式.docx

-

大型实践活动报备申请书doc文档格式.docx

-

高三语文孔雀东南飞课后练习文档格式.docx

-

第十册语文第一乐园文档格式.docx

-

清明节安全主题活动教案文档格式.docx

-

经济法中的反垄断及不正当竞争法规分析 2Word下载.docx

-

公开招标请示范本docWord下载.docx

-

抖音最火的神曲首Word格式文档下载.docx

-

趣味谜语诗看诗人们斗才华你能猜对几个文档格式.docx

-

年春节联欢晚会Word文档下载推荐.docx

-

近似数和有效数字Word文件下载.docx

-

个人健康管理计划书全版docWord文件下载.docx

-

人力资源诊断报告Word文件下载.docx

-

热力管道焊接技术交底Word下载.docx

-

国内外试题库的研究现状分析Word格式.docx

-

固定资产需求文档新增功能文档格式.docx

-

桑植县住房公积金管理中心招聘试题及答案解析Word下载.docx

-

人教版go for it九年级电子课本Word文档格式.docx