西方财务会计课后习题答案.docx

西方财务会计课后习题答案.docx

- 文档编号:3900921

- 上传时间:2022-11-26

- 格式:DOCX

- 页数:73

- 大小:58.22KB

西方财务会计课后习题答案.docx

《西方财务会计课后习题答案.docx》由会员分享,可在线阅读,更多相关《西方财务会计课后习题答案.docx(73页珍藏版)》请在冰豆网上搜索。

西方财务会计课后习题答案

西方财务会计课后习题答案

MerchandiseInventoryandCostof

GoodsSold

CheckPoints

(10min.)CP6-1

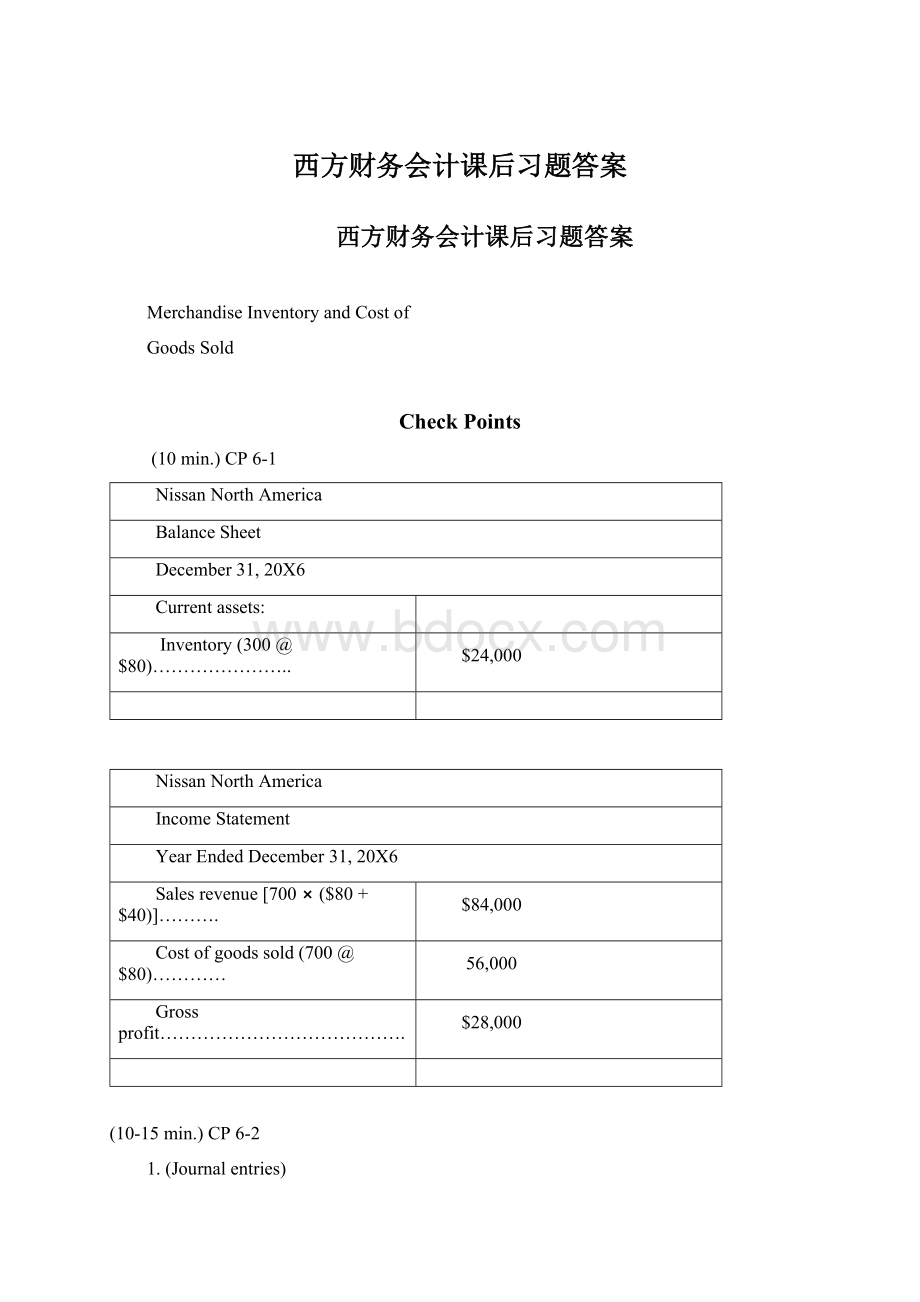

NissanNorthAmerica

BalanceSheet

December31,20X6

Currentassets:

Inventory(300@$80)…………………..

$24,000

NissanNorthAmerica

IncomeStatement

YearEndedDecember31,20X6

Salesrevenue[700⨯($80+$40)]……….

$84,000

Costofgoodssold(700@$80)…………

56,000

Grossprofit………………………………….

$28,000

(10-15min.)CP6-2

1.(Journalentries)

Inventory…………………………………..

100,000

AccountsPayable…………………….

100,000

Cash($140,000⨯.20)……………………

28,000

AmountsReceivable($140,000⨯.80)..

112,000

SalesRevenue………………………...

140,000

CostofGoodsSold……………………..

60,000

Inventory($100,000⨯.60)…………..

60,000

2.(Financialstatements)

BALANCESHEET

Currentassets:

Inventory($100,000–$60,000)……………….

$40,000

INCOMESTATEMENT

Salesrevenue………………………………………

$140,000

Costofgoodssold………………………………..

60,000

Grossprofit…………………………………………

$80,000

(10min.)CP6-3

Billions

Inventory…………………………

6.4

Cash…………………………...

6.4

AccountsReceivable………….

28.5

SalesRevenue……………….

28.5

CostofGoodsSold……………

6.2

Inventory……………………...

6.2

Cash………………………………

26.3

AccountsReceivable……….

26.3

(10min.)CP6-4

1.Inventorycostsareincreasingfrom$10to$14to$18perunit.

2.FIFOresultsinthehighestcostofendinginventory($360)becauseunderFIFOtheendinginventoryiscostedatthelastcostsincurredduringtheperiod.Whencostsareincreasing,thelastcostsarethehighestcosts.

FIFOresultsinthelowestcostofgoodssold.Thisoccursbecausetheoldestcostsareassignedtocostofgoodssold.Whencostsareincreasing,theoldestcostsarethelowest.

FIFOresultsinthehighestgrossprofitbecausecostofgoodssold,theexpense,isthelowest.(Salesrevenueisunaffectedbytheinventorycostingmethod.)

3.LIFOresultsinthelowestcostofendinginventory($240)becauseunderLIFO,theendinginventoryiscostedattheoldestcosts.Whencostsareincreasing,theoldestcostsarethelowestcosts.

LIFOresultsinthehighestcostofgoodssold.Thisoccursbecausethelastcostsoftheperiodareassignedtocostofgoodssold.Whencostsareincreasing,thelastcostsarethehighest.

LIFOresultsinthelowestgrossprofitbecausecostofgoodssold,theexpense,isthehighest.(Salesrevenueisunaffectedbytheinventorycostingmethod.)

(10min.)CP6-5

a

b

c

Average

Cost

FIFO

LIFO

Costofgoodssold:

Average(50@$15*)

$750

FIFO(10@$10)+(25@$14)+(15@$18)

$720

LIFO(25@$18)+(25@$14)

$800

Endinginventory:

Average(10@$15*)

$150

FIFO(10@$18)

$180

LIFO(10@$10)

$100

_____

*Averagecost

=

($100+$350+$450)

=

$15

perunit

(10+25+25)

(10-15min.)CP6-6

Kinko’s

IncomeStatement

YearEndedDecember31,20XX

Average

FIFO

LIFO

Salesrevenue(600⨯$20)

$12,000

$12,000

$12,000

Costofgoodssold(600⨯$9.90*)

5,940

(100⨯$9)+(500⨯$10)

5,900

(600⨯$10)

6,000

Grossprofit

6,060

6,100

6,000

Operatingexpenses

4,000

4,000

4,000

Netincome

$2,060

$2,100

$2,000

_____

*

Beginninginventory(100@$9.20)…………..

$920

Purchases(700@$10)…………………………

7,000

Goodsavailable…………………….……………

$7,920

Averagecostperunit$7,920/800units…

$9.90

(10min.)CP6-7

Kinko’s

IncomeStatement

YearEndedDecember31,20XX

Average

FIFO

LIFO

Salesrevenue(600⨯$20)

$12,000

$12,000

$12,000

Costofgoodssold(600⨯$9.90*)

5,940

(100⨯$9)+(500⨯$10)

5,900

(600⨯$10)

______

______

6,000

Grossprofit

6,060

6,100

6,000

Operatingexpenses

4,000

4,000

4,000

Incomebeforeincometax

$2,060

$2,100

$2,000

Incometaxexpense(40%)

$824

$840

$800

*FromCP6-6

(5min.)CP6-8

Lands’Endmanagerscandelaypurchasesofinventoryuntilthenextyear.UnderLIFO,highinventorycoststhatwouldhavebeenpaidforinventorydonotbecomeexpenseascostofgoodssoldinthecurrentyear.Asaresult,thecurrentyear’sincomestatementreportsahighernetincomethanLands’Endwouldhavereportedifthecompanyhadreplacedinventorybeforeyearend.

(5-10min.)CP6-9

Millions

BALANCESHEET

Currentassets:

Inventories,atmarket(whichislowerthancost)..

$330

INCOMESTATEMENT

Costofgoodssold[$1,001+($333–$330)]…………

$1,004

(10min.)CP6-10

1.FIFO

2.LIFO

Grossprofitpercentage:

Grossprofit

=

$460*

=

46%

$340**

=

34%

Netsalesrevenue

$1,000

$1,000

_____

*$1,000–$540=$460

**$1,000–$660=$340

Inventoryturnover:

Costofgoodssold

=

$540

$660

Averageinventory

($100+$360)/2

($100+$240)/2

=

2.3times

=

3.9times

3.

Grossprofitpercentage—FIFOlooksbetter.

4.

Inventoryturnover—LIFOlooksbetter.

(10-15min.)CP6-11

1.

Beginninginventory……………………………...

$300,000

+

Purchases……………………………………….…

1,600,000

=

Goodsavailable…………………………………...

1,900,000

–

Costofgoodssold……………………………….

(1,800,000)

=

Endinginventory……………………………….…

$100,000

2.

Beginninginventory……………………………..

$300,000

+

Purchases……………………………………….…

s

ame

1,600,000

=

Goodsavailable…………………………………...

1,900,000

–

Costofgoodssold:

Salesrevenue……………………….

$3,000,000

Lessestimatedgrossprofit(40%)

(1,200,000)

Estimatedcostofgoodssold……………….

(1,800,000)

=

Estimatedcostofendinginventory…………...

$100,000

(5-10min.)CP6-12

Correct

Amount(Millions)

a.

Inventory($333+$3)…………………………………

$336

b.

Netsales(unchanged)……………………………….

$1,755

c.

Costofgoodssold($1,001–$3)…………………...

$998

d.

Grossprofit($754+$3)……………………….……..

$757

(10min.)CP6-13

1.Lastyear’sreportedgrossprofitwasunderstated.

Correctgrossprofitlastyearwas$5.6million($4.0+$1.6).

2.Thisyear’sgrossprofitisoverstated.

Correctgrossprofitforthisyearis$3.2million($4.8–$1.6).

3.Lang’sperspectiveisbetterbecausecorrectingtheerrorchangesthetrendofcorrectgrossprofitfromup(good)todown(bad),asfollows:

Millions

LastYear

ThisYear

Trend

Reportedgrossprofit……..

$4.0

$4.8

Up(Good)

Correctgrossprofit……….

$5.6

$3.2

Down(Bad)

(5-10min.)CP6-14

1.Ethical.Thereisnothingwrongwithbuyinginventorywheneveracompanywishes.

2.Ethical.Sameideaas1.

3.Unethical.Thecompanyfalsifieditsreportedamountsofinventoryandnetincome.

4.Unethical.Thecompanyfalsifieditsreportedinventorypurchases,costofgoodssold,andnetincomeinordertocheatthegovernment(andthepeople)outofincometax.

5.Unethical.Thecompanyfalsifieditsreportedamountofinventoryinordertocheatthegovernment(andthepeople)outoftaxes.

Exercises

(15-20min.)E6-1

Req.1(journalentried)

PerpetualSystem

1.

Purchases:

Thousands

Inventory…………………….……….…

2,200

AccountsPayable………………….

2,200

2.

Sales:

Cash($3,500⨯.20)…….……………..

700

AccountsReceivable($3,500⨯.80).

2,800

SalesRevenue…………….……….

3,500

CostofGoodsSold…………………..

2,100

Inventory………………….………....

2,100

Req.2(financialstatementamounts)

BALANCESHEET

Thousands

Currentassets:

Inventory($370+$2,200–$2,100)...

$470

INCOMESTATEMENT

Salesrevenue…………………………….

$3,500

Costofgoodssold………………………

2,100

Grossprofit……………………………….

$1,400

(15-25min.)E6-2

Journal

DATE

ACCOUNTTITLESANDEXPLANATION

DEBIT

CREDIT

1

Inventory($640+$1,870+$900)……….

3,410

AccountsPayable………………………

3,410

2

AccountsReceivable(17@$500)……...

8,500

SalesRevenue…………………………..

8,500

CostofGoodsSold……………………….

2,800*

Inventory…………………………………

2,800

3

Salesrevenue………………………………

$8,500

Costofgoodssold………………………..

2,800

Grossprofit…………………………………

$5,700

Endinginventory($800+$3,410–$2,800)……...

$1,410

_____

*(9@$160)+(8@$170)=$2,800

(10-15min.)E6-3

1.

Inventory

Begin.Bal.

(5units@$160)800

Purchases

Oct.8

(4units@$160)640

15

(11units@$170)1,870

Costofgoodssold

26

(5units@$180)900

(17units@$?

)

?

Endingbal.

(8units@$?

)?

CostofGoodsSold

EndingInventory

(a)Specific

unitcost

(6@$160)+(11@$170)

=

$2,830

(3@$160)+(5@$180)

=

$1,380

(b)Average

cost

17⨯$168.40*

=

$2,863

8⨯$168.40*

=

$1,347

_____

*Averagecostperunit

=

($800+$640+$1,870+$900)

=

$168.40

(5+4+11+5)

(c)FIFO

(9@$160)+(8@$170)

=

$2,800

(5@$180)+(3@$170)

=

$1,410

(d)LIFO

(5@$180)+(11@$170)+(1@$160)

=

$2,930

(8@$160)

=

$1,280

2.LIFOproducesthehighestcostofgoodssold.

FIFOproducesthelowestcostofgoodssold.

Theincreaseininventorycostfrom$160to$170to$180perunit

- 配套讲稿:

如PPT文件的首页显示word图标,表示该PPT已包含配套word讲稿。双击word图标可打开word文档。

- 特殊限制:

部分文档作品中含有的国旗、国徽等图片,仅作为作品整体效果示例展示,禁止商用。设计者仅对作品中独创性部分享有著作权。

- 关 键 词:

- 西方 财务会计 课后 习题 答案

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

转基因粮食的危害资料摘编Word下载.docx

转基因粮食的危害资料摘编Word下载.docx

-

高中英语词组大全Word文档下载推荐.docx

-

卫计局年工作总结及新年工作计划Word格式.docx

-

贵州省煤矿安全管理人员安全资格证A考试概况Word格式.docx

-

系统集成项目招标文件Word文件下载.docx

-

消防设计技术审查的要点Word文档格式.docx

-

第三章 习题课 带电粒子在磁场或复合场中的运动Word格式.docx

-

湖南岳阳中考英语模拟卷含答案Word文档格式.docx

-

电子商务考试题总汇打印版打印打印Word下载.docx

-

选调生考试备考言语理解与表达真题Word文档格式.docx

-

高考物理实验题专练 专练15Word文档格式.docx

-

加装奥迪A4L蓝牙电话功能Word文档下载推荐.docx

-

学年下学期好教育高三月考仿真卷A卷 语文 学生版后附详解Word文档下载推荐.docx

-

净化生产车间工程一般施工技术施工方案Word文档格式.docx

-

内蒙古呼和浩特市第六中学学年高一政治下学期期末考试试题Word下载.docx

-

证券行业客户经理电话营销技巧与实例Word文档下载推荐.docx

-

叶芝 苇间风文档格式.docx

-

最新中美贸易摩擦的原因及解决对策1论文Word文件下载.docx

-

意义的近义词Word格式文档下载.docx

-

上海市中考英语试题S.docx

-

专题12观点论证类设问.docx

-

附加安心重疾条款.docx

-

设计变更管理办法修改意见稿FINAL汇编.docx

-

毕业赠言毕业致词精选多篇.docx

-

银行新员工代表发言稿精选多篇.docx

-

北京市朝阳区届高三第一学期期末语文试题Word版含答案.docx

-

HL线切割使用说明书模板.docx

-

车工实训周记.docx

-

USBHID键盘扫描码.docx

-

Apmpoqu4调研报告.docx

-

最熟悉的陌生人作文八篇.docx

-

被动语态综合讲解.docx

-

砖混结构水电安装施工方案Word文档下载推荐.docx

-

中国国古建筑欣赏与设计柳肃答案Word文档下载推荐.docx

-

个人理财规划宋蔚蔚版尔雅答案.docx

-

新建县天然林资源保护工程项目可行性研究报告Word格式.docx

-

#JAVA学生信息系统97398文档格式.docx

-

材料科学与工程专业英语第三版翻译以及答案.docx

-

新整理我得到了什么作文15篇Word文件下载.docx

-

新人教版四年级上册单元测试题全套Word文档格式.docx

-

小武影视鉴赏拉片笔记Word文档格式.docx

-

小记者如何进行现场采访Word格式文档下载.docx

-

新最新时事政治均衡价格理论的知识点总复习2Word格式.docx

-

新人教版四年级语文上册全册导学案Word文档格式.docx

-

中国王府建筑的艺术特色与保护传承的思考以恭王府为例Word文档格式.docx

-

新小学新标准英语三年级起始单词表Word文档格式.docx

-

信息管理系统MIS设计文档测试计划Word文档格式.docx

-

中国人民银行支行工作总结Word文档格式.docx

-

桩头剔凿施工方案1Word格式.docx

-

《风向和风速》练习修改教学文案Word格式.docx

-

《Visual Foxpro》综合复习资料Word格式文档下载.docx