02第二周Unit1 A Financial Institution.docx

02第二周Unit1 A Financial Institution.docx

- 文档编号:28951130

- 上传时间:2023-07-20

- 格式:DOCX

- 页数:16

- 大小:29.90KB

02第二周Unit1 A Financial Institution.docx

《02第二周Unit1 A Financial Institution.docx》由会员分享,可在线阅读,更多相关《02第二周Unit1 A Financial Institution.docx(16页珍藏版)》请在冰豆网上搜索。

02第二周Unit1AFinancialInstitution

Unit1MoneyandBanking

Part1ReadingandTranslating:

Bank

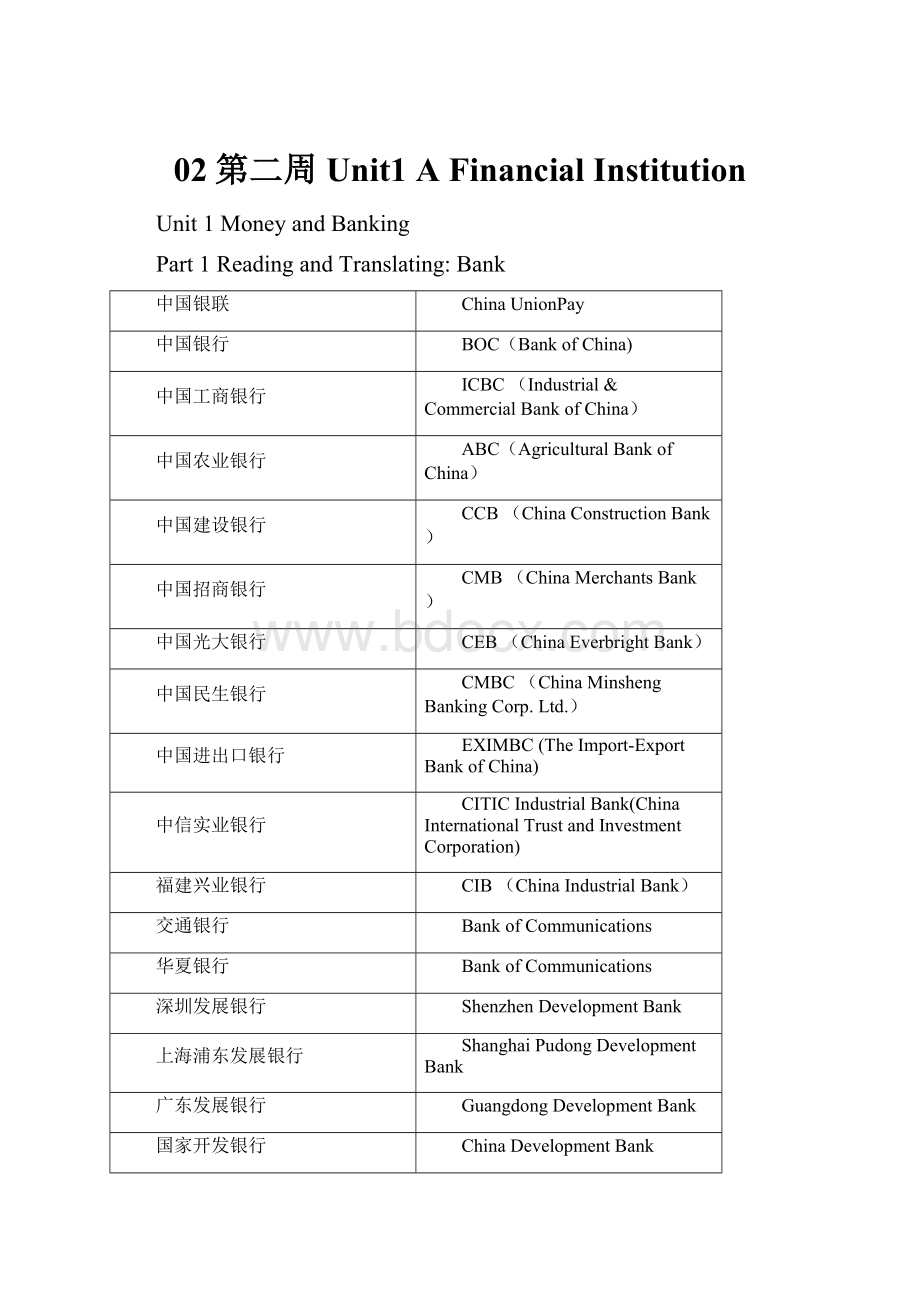

中国银联

ChinaUnionPay

中国银行

BOC(BankofChina)

中国工商银行

ICBC(Industrial&CommercialBankofChina)

中国农业银行

ABC(AgriculturalBankofChina)

中国建设银行

CCB(ChinaConstructionBank)

中国招商银行

CMB(ChinaMerchantsBank)

中国光大银行

CEB(ChinaEverbrightBank)

中国民生银行

CMBC(ChinaMinshengBankingCorp.Ltd.)

中国进出口银行

EXIMBC(TheImport-ExportBankofChina)

中信实业银行

CITICIndustrialBank(ChinaInternationalTrustandInvestmentCorporation)

福建兴业银行

CIB(ChinaIndustrialBank)

交通银行

BankofCommunications

华夏银行

BankofCommunications

深圳发展银行

ShenzhenDevelopmentBank

上海浦东发展银行

ShanghaiPudongDevelopmentBank

广东发展银行

GuangdongDevelopmentBank

国家开发银行

ChinaDevelopmentBank

商业银行

CommercialBank

Jokes:

中国建设银行——CBC(ConstructionBankofChina)——“存不存?

”

中国银行 ——BC(BankofChina)——“不存。

”

中国农业银行——ABC(AgriculturalBankofChina)——“啊,不存”

中国工商银行——ICBC(IndustrialandCommercialBankofChina)——“爱存不存”

中国招商银行 ——CMBC(ChinaMerchantsBank)——“存吗?

?

白痴!

”

兴业银行 ——CIB(IndustrialBank)——“存一百”

北京市商业银行——BCCB(BeijingCityCommercialBank)——白存存不?

”

汇丰银行 ——HSBC(TheHongkongandShanghaiBankingCorporation)还是不存”

FinancialInstitutions:

Theterm“financialintermediary”canbeappliedtoavarietyofinstitutions,someofwhichare

commercialbanks

商业银行

mutualsavingsbanks

互助储蓄银行

savingsandloanassociations

储蓄贷款协会

creditunions

信用社

lifeinsurancecompanies

人寿保险公司

pensionfunds

养老基金

mutualfunds

互助基金

financecompanies

金融公司

governmentalcreditagencies

政府借贷机构

InsuranceCompanies:

中国人寿保险股份有限公司

ChinaLifeInsuranceCompanyLimited

中国人民财产保险股份有限公司

PICCPropertyandCasualtyCompanyLimited

天安保险股份有限公司

TiananInsuranceCo.,Ltd

中国太平洋保险(集团)股份有限公司

ChinaPacificInsurance(group)Co.,Ltd

新华人寿保险股份有限公司

NewChinaLifeInsuranceCo.,Ltd.

华夏人寿保险股份有限公司

HuaxiaLifeInsuranceCo.Ltd

Part2:

VocabularyandUsefulExpressions

Part3:

TextReading

1.Definition:

Financialinstitutionsorfinancialintermediariesareverysimplyeconomicunitswhosemainfunctionistohandlethefinancialassetsofhouseholdsandfirmsinoursociety.Basically,theseinstitutionsbringsaversandborrowerstogetherbysellingsecuritiestosaversformoneyandlendingthatmoneytoborrowers.

2.Characteristics:

1)Firstly,financialintermediariescouldnotexistwithoutintermediation,theprocessthatoccurswhenfirmsandhouseholdsplacefundsininstitutions(banks,savingsandloans,etc.).

2)Anotherimportantattributeoffinancialintermediariesistheirabilitytobearandspreadtheriskofprimarysecurityownership.Financialintermediariesaremoreeasilyabletodiversifytheirsecurityportfolios,therebyreducingthetotalriskoftheportfolio.Lower-than-expectedreturnsononeissuemaybeoffsetbyhigher-than-expectedreturnsonanother.

3)Anotherinterestingattributeoffinancialintermediariesistheirabilitytooffsetreceiptsandwithdrawalsbecauseofthephenomenonofthe“lawoflargenumber”

3.Conclusion:

Itshouldbeapparentthatfinancialintermediariesfacilitateamoreefficientflowoffundsfromlenderstoborrowers.Itshouldalsobeapparentthatthisloweringofinterestrateswouldbehighlybeneficialtoacountry’srateofeconomicgrowthanddevelopment.

Part4:

Relatedtexts

(一)中国银行业改革面临倒退危险

WhileWesterngovernmentsdebatehowtoreformtheirbankingsectors,Beijingisnowfacingadifferentproblem:

howtokeepfromguttingthelastdecadeofbankingreformit'salreadybeenthrough.There'saveryrealdangerthatpolicymakerswillundotheirearliereffortsinthenameofshort-termstimulus.

眼下,在西方国家政府争论应如何改革它们的银行体系之际,中国政府却面临着一个不同的问题:

如何避免让它过去10年来已获得的改革成果前功尽弃。

现在的确存在着一种危险,即:

决策者有可能在短期刺激计划的名义下毁掉他们早些时候做出的努力。

ThecentralproblemistheChinesegovernment'sstrategyofstimulatingtheeconomythroughanenormousexpansionofbanklending.Thegovernmenthasturnedtothebankstofinancehalfofitsfourtrillionyuan($586billion)stimuluspackage.Inadditiontothat,thegovernmenthassethightargetsforcommerciallendingtosupportbusinesses.China'slenderspumpedoutmorethan4.5trillionyuaninnewloansinthefirstquarterof2009,8%morethaninallof2008.

问题的核心是中国政府正在实行的通过大规模扩大银行信贷来刺激经济的策略。

政府4万亿元人民币(合5,860亿美元)经济刺激计划的一半资金都有赖银行提供。

除此之外,政府还为支持企业的商业借贷制定了高目标。

今年一季度,中国银行业新增贷款超过4.5万亿元,较2008年全年的数字还高出8%。

Thisiseerilyreminiscientofanearliererawhenthegovernmentleanedheavilyonbankstofinanceeconomicgrowth,andespeciallylargestate-ownedenterprises.Inthe1980sand'90s,Chinesebankspiledupacolossaltangleofpoliticallydirectedbaddebtsthateithercouldnotberepaid,orwerenevermeanttoberepaidinthefirstplace.In2003nonperformingloansmadeup20.4%ofbanks'totalloanbooks,afacevalueequivalentto16.5%ofGDP.Thisthreatenedtoswamptheentireeconomy.

这种局面会令人不禁回想起前些年的情形,当时中国政府严重依赖银行资金来支撑经济增长,特别是大型国有企业的发展。

上世纪八、九十年代,中国银行业积累了大量行政指令导致的呆坏帐,这些债务要么没法得到偿还,要么当初就根本没打算偿还。

2003年,不良贷款占中国银行业贷款总额的20.4%,相当于中国国内生产总值(GDP)的16.5%。

如此之高的坏帐让整个中国经济面临着陷入困境的危险。

BeijingmanagedtocleanupthatproblemwiththehelpofthenewChinaBankingRegulatoryCommission,$100billioninnewgovernmentcapital,andforeign'strategicpartners'totrainbanksinglobalbestpractices.Nonperformingloanswerebroughtdownto2.5%bytheendof2008.Thiswasaccompaniedbyadeeperchangeincorporateculture,asbankstaffstartedthinkinglikebankersinsteadoflikeagentsofgovernmentpolicy.AdecadeofdifficultreformculminatedinHongKongstocklistingsforthreeofthebigfour--BankofChina,IndustrialandCommercialBankofChinaandChinaConstructionBank--withthefourth,AgriculturalBankofChina,ontheway.Yetdespitethishard-wonprogress,Beijingisnowindangerofbacksliding.

中国政府后来设法扭转了这种局面,当时,中国新成立了银行业监督管理委员会(ChinaBankingRegulatoryCommission),政府又拿出1,000亿美元资金注入银行业,此外,还通过外国“战略合作伙伴”向中国银行业传授全球最佳经营管理规范。

到2008年末,不良贷款比率降到了2.5%。

与此同时,中国银行业在企业文化方面也发生着更深层的变化。

银行业人士开始像银行家而不是像政府官员那样来考虑问题。

经过十年的艰苦改革,中国四大国有银行中的三家──中国银行(BankofChina)、中国工商银行(IndustrialandCommercialBankofChina)和中国建设银行(ChinaConstructionBank)──先后在香港挂牌上市,中国农业银行(AgriculturalBankofChina)的上市工作也在进行中。

然而,在取得这番来之不易的进步之后,中国的银行业改革现在面临着倒退的危险。

Onthesurface,China’sbanksappeartoberemarkablyhealthy.TheCBRCreportsthatthisyear,despitetheeconomicslowdown,nonperformingloanshavecontinuedfalling,notonlyasapercentageoftherapidlyexpandingbasebutinabsoluteterms.China'sbanks,thestorygoes,areawell-tunedenginecapableofliftingtheChineseeconomyup.

从表面上看,中国银行业似乎已经相当健康。

据银监会称,尽管经济出现下滑,但今年银行业不良贷款将继续下降,不论是绝对规模,还是占贷款总额的比例。

看上去,中国银行业俨然是一台运转良好、有能力继续推动中国经济前行的发动机。

Acloserlook,however,raisesseveralredflagsthatregulatorshaven'tbeenabletoaddresssatisfactorily.Takeexistingloanportfoliosevenbeforetherashofnewstimuluslending.Giventheseveredrop-offinChineseexports,alongwiththeworldwidewideningofcreditspreads(reflectingincreasedriskofdefaults),itstrainscredulitytobelievethatthehealthoftheseportfolioscouldbeimproving.Inreality,theCBRCrecentlyallowedChinesebankstominimizetherecognitionofnonperformingloansbyreschedulingloansbeforematurityand'evergreening'troubledloansbyrollingthemoverintonewones.Incontrast,NPLsrecognizedbyforeignbanksoperatinginChina--whichgenerallyfollowthestricterrulesoftheirhomeregulators--havemorethandoubledsincethestartof2008.

不过,进一步研究会发现,中国银行业还存在几个监管机构尚未能妥善解决的问题。

就以银行业大规模发放新的刺激性贷款之前已存在的贷款组合来说。

鉴于中国出口的大幅下滑,还有全世界范围内信用价差的扩大(这意味着违约风险的上升),人们很难轻易相信这些贷款组合的质量还能不断改善。

事实上,银监会最近已允许中国银行业对未到期贷款重新安排偿债条款,将不良贷款展期成为不到期的新贷款,从而降低列为不良贷款的贷款额。

相比之下,在华经营的外资银行认定的不良贷款自2008年初以来已经增加了一倍多。

这些银行一般都会遵守他们本国监管机构的严格规定。

(二)中国影子银行隐藏的风险《金融时报》双语新闻

WithinafewminutesofdrivingintoLangfang,itisclearthatChina’spropertyboomisstillgoingstrong.Atatrafficlight,atoutknocksonthecarwindowwithaleafletadvertisinganewhousingdevelopment,LionCity.Asecondleaflet–forthesprawling19CityStatesvillacomplex–isinsertedunderthewindscreenwiper,followedquicklybyathird,forHappyCity.

驱车驶入廊坊,不出几分钟就能感受到中国房地产市场繁荣依旧。

等待红灯时,一位推销员敲打着我的车窗,手里拿着一张新开发楼盘“狮子城”的小广告。

第二张小广告被插到了风挡雨刷上,是“旭辉十九城邦”的,接着又有张“幸福城”的小广告插了上来。

Ared-hothousingmarketmightnotseemunusualinChina,whererealestatepriceshavesoaredoverthepastdecade.ButwhatishappeninginLangfang,onehour’sdrivefromBeijing,andothercitiesisnewandpotentiallyfarriskierthananythingthatcameearlier.Since2010,thegovernmenthastriedtocoolthepropertymarketandmadeitvirtuallyimpossiblefordeveloperstosecureloansfrombanks.Starvedofcash,developerswereforcedtoslowdown.

火爆的楼市在中国可能不算罕见,毕竟过去十年中国房地产价格已经大幅攀升。

然而,在距北京一小时车程的廊坊以及其他城市正在出现一种新的现象,其中隐含的风险比起早先任何情况都要大得多。

2010年以来,中国政府已经试图给楼市降温,导致开发商几乎不可能从银行获得贷款。

由于缺乏资金,开发商不得不放慢开发节奏。

ButastheLangfangboomshows,propertycompaniesarefindingfundsagain.Themoneyisnotcomingfrombanksastheregulatorycontrolsonloanstodevelopersremain.Instead,developersareturningtoChina’sshadowbankingsystem,acomplexnetworkoffinancingchannelsoutsidetheformalbankingsector.

然而廊坊房市的繁荣说明地产公司又找到了资金。

开发商的资金并不是来自银行,因为监管机构对于向开发商发放的贷款依然严格控制。

相反,开发商们正转而求助于中国的影子银行系统——一个由游离于正规银行部门之外的融资渠道组成的复杂网络。

ShadowbankingisflourishinginChina,helpingtomakenon-bankinstitutionsasbigasourceofcreditasbanksthemselvessinceJuly–somethingthathasneverhappenedbefore.Chinesebankers,leadingratingagenciesandtheInternationalMonetaryFundhaveallwarnedaboutrisksfromthesurgeinlooselyregulatedlending,withsomeevenpointingtoparallelswithdevelopedeconomiesbeforetheglobalfinancialcrisis.ButtheChinesegovernmentitselfhastakenapermissivestance.

影子银行在中国的繁荣,导致非银行类机构自7月以来成为与银行一样的主要信贷源头——这在过去是从未有过的。

中国银

- 配套讲稿:

如PPT文件的首页显示word图标,表示该PPT已包含配套word讲稿。双击word图标可打开word文档。

- 特殊限制:

部分文档作品中含有的国旗、国徽等图片,仅作为作品整体效果示例展示,禁止商用。设计者仅对作品中独创性部分享有著作权。

- 关 键 词:

- 02第二周Unit1 Financial Institution 02 第二 Unit1

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

#2机组现场施工用电布置措施.docx

#2机组现场施工用电布置措施.docx

-

《个人贵金属质押借款合同》兴业银行.docx

-

《科学发展观和小康社会的经济建设》复习导学案.docx

-

《我和祖父的园子》第一课时教案两篇word.docx

-

《质量》教学案例与设计.docx

-

2惠农小册子.docx

-

7A版个人与团队模拟考试题及答案.docx

-

10篇新部编四年级下册语文课内外阅读理解专项练习题及答案.docx

-

16初四物理热和能知识点总结精讲.docx

-

20XX社会语言经典语录流行风暴.docx

-

48篇教学案例分析报告题.docx

-

《电子工厂安全管理制度汇总》.docx

-

《机械制造课程设计》指导.docx

-

《钱学森》教案第二课时.docx

-

《边城》读后感5篇.docx

-

《固定式压力容器安全技术监察规程》.docx

-

《论雷峰塔的倒掉》.docx

-

《手术台就是阵地》教学设计三年级语文下册.docx

-

《夏洛的网》课外阅读教学设计.docx

-

《自己的花是让别人看的》教案.docx

-

3C检查表090429.docx

-

7客运专线CRTSⅡ型板式无砟轨道施工工法.docx

-

《笔算除法》课时教案设计.docx

-

11#楼高大模板支撑体系专项方案.docx

-

17科学分析经济形势.docx

-

《电流和电路》易错题精讲综合检测题与答案.docx

-

《会计信息系统》习题含答案.docx

-

《汽车电器设备与维修》发电机分教考分离试题及标准答案.docx

-

《四川省排污许可证管理暂行办法》.docx

-

《新编实用英语》教案第一册Unit.docx

-

0母版锅炉值班员计算题WORD版.docx

-

3年级下册英语单词记忆人教版.docx

-

Speaking of ielts.docx

-

Unit8haveyoureadtreasureislandyet.docx

-

WPS文字操作技巧.docx

-

XX国际酒店公寓热泵工程设计实施项目可行性方案.docx

-

XX省现代农机合作社建设项目可行性方案.docx

-

X年甲硝唑药品销售数据市场调研报告.docx

-

安徽省滁州市定远县育才学校学年高二地理下学期期末考试试题实验.docx

-

安全管理课程考试题集.docx

-

安全生产月方案.docx

-

澳洲留学三方合作协议书.docx

-

八年级英语上册第二单元重要考点归纳人教版.docx

-

白菜肉包早餐菜谱.docx

-

班主任实习工作计划.docx

-

钣金件结构设计知识.docx

-

保姆合同8篇.docx

-

北京高三一模各区合集26题.docx

-

0622G17深基坑监测周报1.docx

-

A6包海洋环境监测仪器设备烟台1.docx

-

CAD理论测验练习题.docx