《会计英语》课后习题答案.docx

《会计英语》课后习题答案.docx

- 文档编号:2870880

- 上传时间:2022-11-16

- 格式:DOCX

- 页数:22

- 大小:227.24KB

《会计英语》课后习题答案.docx

《《会计英语》课后习题答案.docx》由会员分享,可在线阅读,更多相关《《会计英语》课后习题答案.docx(22页珍藏版)》请在冰豆网上搜索。

《会计英语》课后习题答案

SuggestedSolution

Chapter1

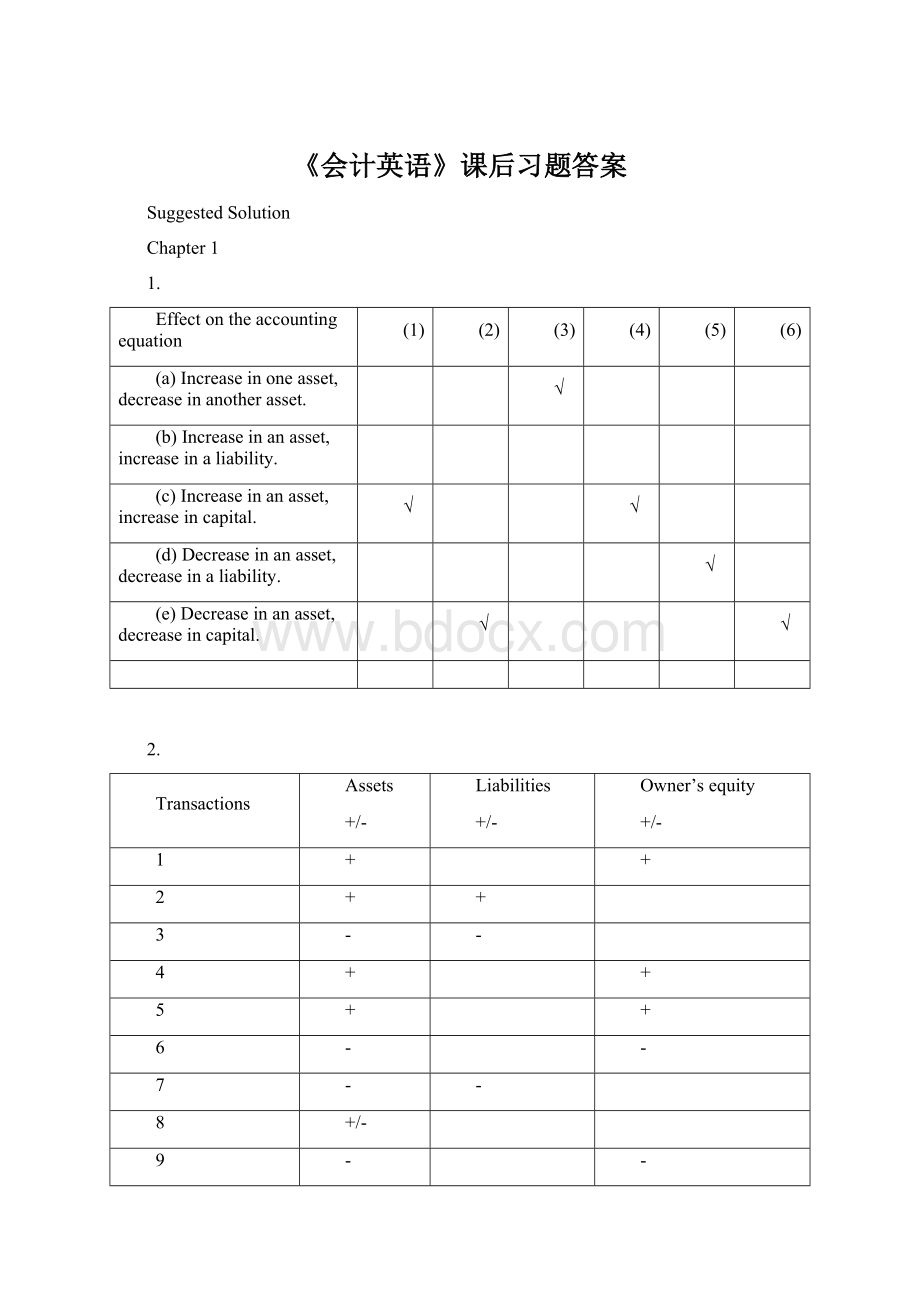

1.

Effectontheaccountingequation

(1)

(2)

(3)

(4)

(5)

(6)

(a)Increaseinoneasset,decreaseinanotherasset.

√

(b)Increaseinanasset,increaseinaliability.

(c)Increaseinanasset,increaseincapital.

√

√

(d)Decreaseinanasset,decreaseinaliability.

√

(e)Decreaseinanasset,decreaseincapital.

√

√

2.

Transactions

Assets

+/-

Liabilities

+/-

Owner’sequity

+/-

1

+

+

2

+

+

3

-

-

4

+

+

5

+

+

6

-

-

7

-

-

8

+/-

9

-

-

10

-

-

3.

Describeeachtransactionbasedonthesummaryabove.

Transactions

1

Purchasedlandforcash,$6,000.

2

Investmentforcash,$3,200.

3

Paidexpense$1,200.

4

Purchasedsuppliesonaccount,$800.

5

Paidowner’spersonaluse,$750.

6

Paidcreditor,$1,500

7

Suppliesusedduringtheperiod,$630.

4.

Assets

Liabilities

Equity

Beginning

275,000

80,000

195,000

Add.investment

48,000

Add.Netincome

27,000

Lesswithdrawals

-35,000

Ending

320,000

85,000

235,000

5.

(a)

March31,20XX

April30,20XX

Assets

Cash

4,500

5,400

Accountsreceivable

2,560

4,100

Supplies

840

450

Totalassets

7,900

9,950

Liabilities

Accountspayable

430

690

Equity

TinaPierce,Capital

7,470

9,260

(b)netincome=9,260-7,470=1,790

(c)netincome=1,790+2,500=4,290

Chapter2

1.

a.ToincreaseNotesPayable-CR

b.TodecreaseAccountsReceivable-CR

c.ToincreaseOwner,Capital-CR

d.TodecreaseUnearnedFees-DR

e.TodecreasePrepaidInsurance-CR

f.TodecreaseCash-CR

g.ToincreaseUtilitiesExpense-DR

h.ToincreaseFeesEarned-CR

i.ToincreaseStoreEquipment-DR

j.ToincreaseOwner,Withdrawal-DR

2.

a.

Cash

1,800

Accountspayable

1,800

b.

Revenue

4,500

Accountsreceivable

4,500

c.

Owner’swithdrawals

1,500

SalariesExpense

1,500

d.

AccountsReceivable

750

Revenue

750

3.

PrepareadjustingjournalentriesatDecember31,theendoftheyear.

Advertisingexpense

600

Prepaidadvertising

600

Insuranceexpense(2160/12*2)

360

Prepaidinsurance

360

Unearnedrevenue

2,100

Servicerevenue

2,100

Consultantexpense

900

Prepaidconsultant

900

Unearnedrevenue

3,000

Servicerevenue

3,000

4.

1.$388,400

2.$22,520

3.$366,600

4.$21,800

5.

1.netlossfortheyearendedJune30,2002:

$60,000

2.DRJonNissen,Capital60,000

CRincomesummary60,000

3.post-closingbalanceinJonNissen,CapitalatJune30,2002:

$54,000

Chapter3

1.DundeeRealtybankreconciliation

October31,2009

Reconciledbalance$6,220Reconciledbalance$6,220

2.April7Dr:

Notesreceivable—Acompany5400

Cr:

Accountsreceivable—Acompany5400

12Dr:

Cash5394.5

Interestexpense5.5

Cr:

Notesreceivable5400

June6Dr:

Accountsreceivable—Acompany5533

Cr:

Cash5533

18Dr:

Cash5560.7

Cr:

Accountsreceivable—Acompany5533

Interestrevenue27.7

3.(a)Asawhole:

theendinginventory=685

(b)appliedseparatelytoeachproduct:

theendinginventory=625

4.Thecostofgoodsavailableforsale=endinginventory+thecostofgoods=80,000+200,000*500%=80,000+1,000,000=1,080,000

5.

(1)24,000+60,000-90,000*0.8=12000

(2)(60,000+24,000)/(85,000+31,000)*(85,000+31,000-90,000)=18828

Chapter4

1.(a)second-yeardepreciation=(114,000–5,700)/5=21,660;

(b)second-yeardepreciation=8,600*(114,000–5,700)/36,100=25,800;

(c)first-yeardepreciation=114,000*40%=45,600

second-yeardepreciation=(114,000–45,600)*40%=27,360;

(d)second-yeardepreciation=(114,000–5,700)*4/15=28,880.

2.(a)weighted-averageaccumulatedexpenditures(2008)=75,000*12/12+84,000*9/12+180,000*8/12+300,000*7/12+100,000*6/12=483,000

(b)interestcapitalizedduring2008=60,000*12%+(483,000–60,000)*10%=49,500

3.

(1)depreciationexpense=30,000

(2)bookvalue=600,000–30,000*2=540,000

(3)depreciationexpense=(600,000–30,000*8)/16=22,500

(4)bookvalue=600,000–30,000*8–22,500=337,500

4.Situation1:

Jan1st,2008InvestmentinM260,000

Cash260,000

June30Cash6000

Dividendrevenue6000

Situation2:

January1,2008InvestmentinS81,000

Cash81,000

June15Cash10,800

InvestmentinS10,800

December31InvestmentinS25,500

InvestmentRevenue25,500

5.a.December31,2008InvestmentinK1,200,000

Cash1,200,000

June30,2009DividendReceivable42,500

DividendRevenue42,500

December31,2009Cash42,500

DividendReceivable42,500

b.December31,2008InvestmentinK1,200,000

Cash1,200,000

December31,2009Cash42,500

InvestmentinK

- 配套讲稿:

如PPT文件的首页显示word图标,表示该PPT已包含配套word讲稿。双击word图标可打开word文档。

- 特殊限制:

部分文档作品中含有的国旗、国徽等图片,仅作为作品整体效果示例展示,禁止商用。设计者仅对作品中独创性部分享有著作权。

- 关 键 词:

- 会计英语 会计 英语 课后 习题 答案

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

如何打造酒店企业文化2刘田江doc.docx

如何打造酒店企业文化2刘田江doc.docx

-

律师提供著作权法律服务业务操作指引.docx

-

18秋福建师范大学《经济法》在线作业一.docx

-

施工现场危险源.docx

-

山东省潍坊市昌乐县学年七年级地理下学期期中学业质量评估试题.docx

-

新视野大学英语视听说教程第二版第一册完整答案.docx

-

精校版重庆市 初中毕业水平暨高中招生考试中考英语试题AB卷Word版含答案解析.docx

-

新视野大学英语视听说教程第二版第一册完整答案.docx

-

江苏省刘国钧中学1112学年高二语文上学期期末考前辅导试题卷苏教版会员独享.docx

-

山东省潍坊市昌乐县学年七年级地理下学期期中学业质量评估试题.docx

-

西安交通大学18年课程考试《管理会计》作业考核试题.docx

-

施工安全保证体系.docx

-

南开17秋学期《科学启蒙尔雅》在线作业2.docx

-

秋福师《大学英语1》在线作业二.docx

-

231695 北交《运输物流管理》在线作业2 15秋答案.docx

-

梁原学区安全管理工作实施方案.docx

-

环保管理台帐明细.docx

-

我国三大翻译证书考试概览.docx

-

东大17秋学期《大学英语二》在线作业31.docx

-

静态分析指标.docx

-

山东金瀚控股金瀚置业绩效考核指标库.docx

-

B0301A国际贸易.docx

-

人教版八年级数学上册同步练习试题及答案第11章《三角形》 同步练习及答案111.docx

-

秋福师《概率论》在线作业二.docx

-

17秋福师《高级英语阅读二》在线作业一.docx

-

西南大学17秋0764《工程建设监理》在线作业参考资料.docx

-

生活宝典之社会大转盘一.docx

-

专卖店管理.docx

-

100个CFO的八年之资金管理篇.docx

-

东北师范古代汉语三16秋在线作业2.docx

-

专业技术人员公共危机管理考试.docx

-

东大17秋学期《大学英语二》在线作业31.docx

-

卷烟行业市场营销学 1.docx

-

开张大吉祝福语.docx

-

科技局信访工作总结共3篇.docx

-

课标通用安徽省201x年中考化学总复习 分析与备考策略指导.docx

-

口腔组织病理学唾液腺疾病.docx

-

集成电路设计实验报告.docx

-

垃圾分类活动方案精选5篇.docx

-

计算机基础知识38939.docx

-

老人赡养协议书标准版.docx

-

计算机专业毕业生求职信.docx

-

寄语大全之向红旗寄语.docx

-

礼仪知识.docx

-

家庭网络设计.docx

-

沥青路面及乳化沥青施工方法.docx

-

驾校科目训练操作规程.docx

-

梁式转换层施工方案.docx

-

简短的个人年终工作总结5篇.docx

-

临床执业医师模拟459.docx

-

建设工程质量检测人员地基基础低应变法声波透射法.docx