十五 Asset Valuation Debt Investments Analysis and Valuation.docx

十五 Asset Valuation Debt Investments Analysis and Valuation.docx

- 文档编号:28345526

- 上传时间:2023-07-10

- 格式:DOCX

- 页数:27

- 大小:66.40KB

十五 Asset Valuation Debt Investments Analysis and Valuation.docx

《十五 Asset Valuation Debt Investments Analysis and Valuation.docx》由会员分享,可在线阅读,更多相关《十五 Asset Valuation Debt Investments Analysis and Valuation.docx(27页珍藏版)》请在冰豆网上搜索。

十五AssetValuationDebtInvestmentsAnalysisandValuation

十五AssetValuation:

DebtInvestments:

AnalysisandValuation

1.A:

IntroductiontotheValuationofFixedIncomeSecurities

a:

Describethefundamentalprinciplesofbondvaluation.

Bondinvestorsarebasicallyentitledtotwodistincttypesofcashflows:

1)theperiodicreceiptofcouponincomeoverthelifeofthebond,and2)therecoveryofprincipal(parvalue)attheendofthebond'slife.Thus,invaluingabond,you'redealingwithanannuityofcouponpayments,plusalargesinglecashflow,asrepresentedbytherecoveryofprincipalatmaturity,orwhenthebondisretired.Thesecashflows,alongwiththerequiredrateofreturnontheinvestment,arethenusedinapresentvaluebasedbondmodeltofindthedollarpriceofabond.

b:

Explainthethreestepsinthevaluationprocess.

Thevalueofanyfinancialassetcanbedeterminedasthesumoftheasset’sdiscountedcashflows.Therearethreesteps:

∙Estimatethecashflows.

∙Determinetheappropriatediscountrate.

∙Calculatethesumofpresentvaluesoftheestimatedcashflows.

c:

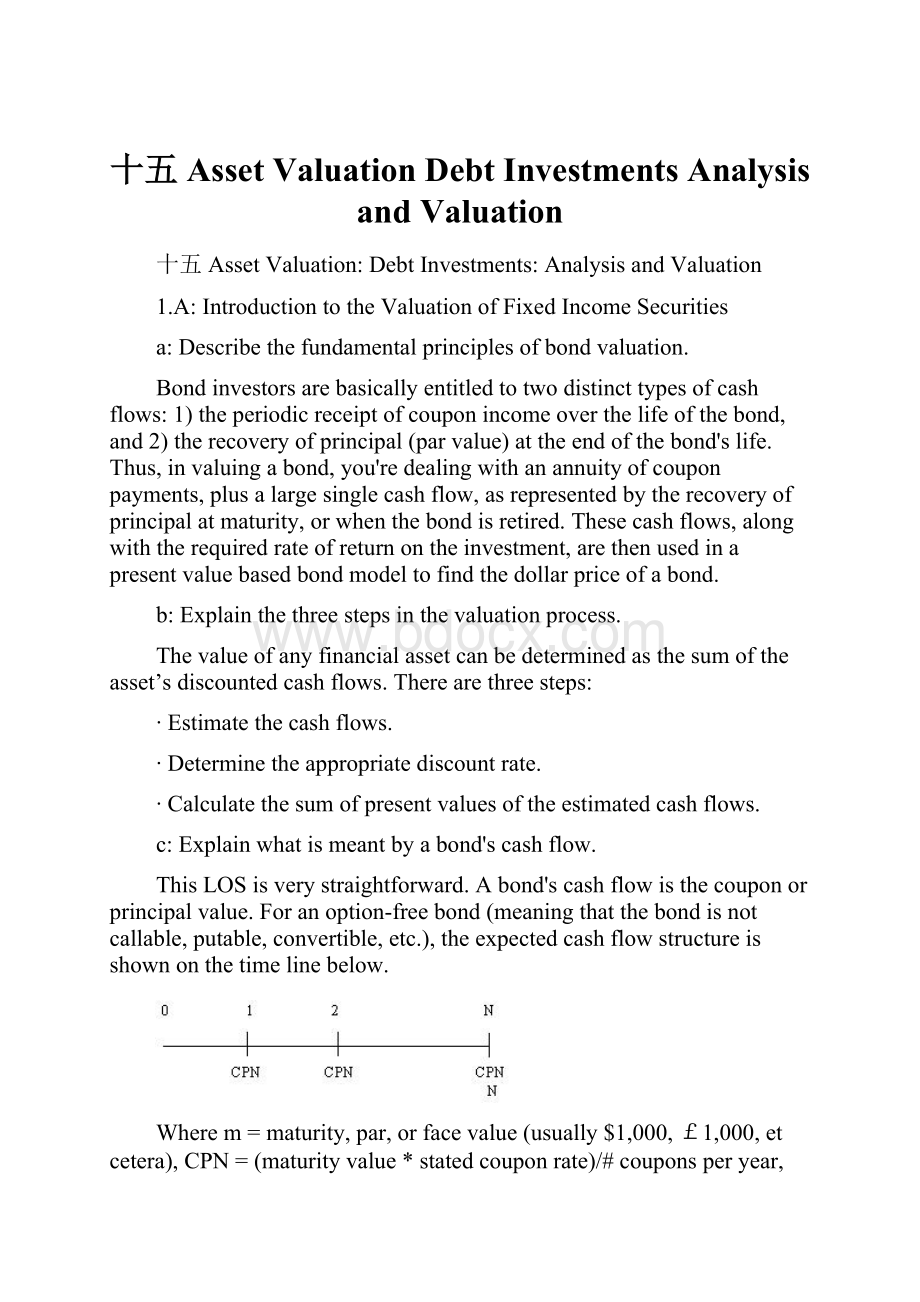

Explainwhatismeantbyabond'scashflow.

ThisLOSisverystraightforward.Abond'scashflowisthecouponorprincipalvalue.Foranoption-freebond(meaningthatthebondisnotcallable,putable,convertible,etc.),theexpectedcashflowstructureisshownonthetimelinebelow.

Wherem=maturity,par,orfacevalue(usually$1,000,£1,000,etcetera),CPN=(maturityvalue*statedcouponrate)/#couponsperyear,andN=#ofyearstomaturity*#couponsperyear.So,foranarbitrarydiscountratei,thebond’svalueis:

Bondvalue=

CPN1

+

CPN2

+...+

CPNn*m+M

(l+i/m)1

(1+i/m)2

(l+i/m)n*m

Where:

i=interestrateperannum(yieldtomaturityorYTM),m=numberofcouponsperyear,andn=numberofyearstomaturity.

d:

Discussthediffultiesofestimatingtheexpectedcashflowsforsometypesofbondsandidentifythebondsforwhichestimatingtheexpectedcashflowsisdifficult.

Normally,estimatingthecashflowstreamofahigh-qualityoption-freebondisrelativelystraightforward,astheamountandtimingofthecouponsandprincipalpaymentsareknownwithahighdegreeofcertainty.Removethatcertainty,anddifficultieswillariseinestimatingthecashflowstreamofabond.Asidefromnormalcreditrisks,thefollowingthreeconditionscouldleadtodifficultiesinforecastingthefuturecashflowstreamofevenhigh-qualityissues:

∙Thepresenceofembeddedoptions,suchascallfeaturesandsinkingfundprovisions-inwhichcase,thelengthofthecashflowstream(lifeofthebond)cannotbedeterminedwithcertainty.

∙Theuseofavariable,ratherthanafixed,couponrate-inwhichcase,thefutureannualorsemi-annualcouponpaymentscannotbedeterminedwithcertainty.

∙Thepresenceofaconversionorexchangeprivilege,soyou'redealingwithaconvertible(orexchangeable)bond,ratherthanastraightbond-inwhichcase,it'sdifficulttoknowhowlongitwillbebeforethebondisconvertedintostock.

e:

Computethevalueofabond,giventheexpectedcashflowsandtheappropriatediscountrates.

Example:

Annualcoupons.Supposethatwehavea10-year,$1,000parvalue,6%annualcouponbond.Thecashvalueofeachcouponis:

CPN=($1,000*0.06)/1=$60.Thevalueofthebondwithayieldtomaturity(interestrate)of8%appearsbelow.Onyourfinancialcalculator,N=10,PMT=60,FV=1000,I/Y=8;CPTPV=865.80.Thisvaluewouldtypicallybequotedas86.58,meaning86.58%ofparvalue,or$865.80.

Bondvalue=[60/(1.08)1]+[60/(1.08)2]+[60+100/(1.08)3]=$865.80

Example:

Semiannualcoupons.Supposethatwehavea10-year,$1,000parvalue,6%semiannualcouponbond.Thecashvalueofeachcouponis:

CPN=($1,000*0.06)/2=$30.Thevalueofthebondwithayieldtomaturity(interestrate)of8%appearsbelow.Onyourfinancialcalculator,N=20,PMT=30,FV=1000,I/Y=4;CPTPV=864.10.Notethatthecouponsconstituteanannuity.

BondValue=

n*m

∑

t=1

30

(1+0.08/2)t

+

1000

(1+0.08/2)n*m

=864.10

f:

Explainhowthevalueofabondchangesifthediscountrateincreasesordecreasesandcomputethechangeinvaluethatisattributabletotheratechange.

Therequiredyieldtomaturitycanchangedramaticallyduringthelifeofabond.Thesechangescanbemarketwide(i.e.,thegenerallevelofinterestratesintheeconomy)orspecifictotheissue(e.g.,achangeincreditquality).However,forastandard,option-freebondthecashflowswillnotchangeduringthelifeofthebond.Changesinrequiredyieldarereflectedinthebond’sprice.

Example:

changesinrequiredyield.Usingyourcalculator,computethevalueofa$1,000parvaluebond,withathreeyearlife,paying6%semiannualcouponstoaninvestorwitharequiredrateofreturnof:

3%,6%,and12%.

AtI/Y=3%/2;n=3*2;FV=1000;PMT=60/2;computePV=-1,085.458

AtI/Y=6%/2;n=3*2;FV=1000;PMT=60/2;computePV=-1,000.000

AtI/Y=12%/2;n=3*2;FV=1000;PMT=60/2;computePV=-852.480

g:

Explainhowthepriceofabondchangesasthebondapproachesitsmaturitydateandcomputethechangeinvaluethatisattributabletothepassageoftime.

Abond’svaluecandiffersubstantiallyfromitsmaturityvaluepriortomaturity.However,regardlessofitsrequiredyield,thepricewillconvergetowardmaturityvalueasmaturityapproaches.Returningtoour$1,000parvaluebond,withathree-yearlife,paying6%semi-annualcoupons.Herewecalculatethebondvaluesusingrequiredyieldsof3,6,and12%asthebondapproachesmaturity.

TimetoMaturity

YTM=3%

YTM=6%

YTM=12%

3.0years

1,085.458

1,000.000

852.480

2.5

1,071.740

1,000.000

873.629

2.0

1,057.816

1,000.000

896.047

1.5

1,043.683

1,000.000

919.810

1.0

1,029.338

1,000.000

944.998

0.5

1,014.778

1,000.000

971.689

0.0

1,000.000

1,000.000

1,000.000

h:

Computethevalueofazero-couponbond.

Youfindthepriceormarketvalueofazerocouponbondjustlikeyoudoacoupon-bearingsecurity,except,ofcourse,youignorethecouponcomponentoftheequation.Theonlycashflowisrecoveryofparvalueatmaturity.Thusthepriceormarketvalueofazerocouponbondissimplythepresentvalueofthebond'sparvalue.

Bondvalue=M/(1+i/m)n*m

Example:

Azerocouponbond.Supposewehavea10-year,$1,000parvalue,zerocouponbond.Tofindthevalueofthisbondgivenitsbeingpricetoyield8%(compoundedsemiannually),you'ddothefollowing:

Bondvalue=1000/(1+.08/2)10*2=456.39

Onyourfinancingcalculator,N=10*2=20,FV=1000,I/Y=8/24;CPTPV=456.39(ignorethesign).

Thedifferencebetweenthe$456.39andtheparvalue($1000)istheamountofinterestthatwillbeearnedoverthe10-yearlifeoftheissue.

i:

Computethedirtypriceofabond,accruedinterest,andcleanpriceofabondthatisbetweencouponpayments.

Assumewearetryingtopricea3-year,$1,000parvalue,6%semiannualcouponbond,withYTM=12%,withamaturityofJanuary15,2005,andyouarevaluingthebondforsettlementonApril20,2002.ThenextcouponisdueJuly15,2002.Therefore,thereare85daysbetweensettlementandnextcoupon,and180daysinthecouponperiod.Thefractionalperiod(w)=85/180=0.4722.Thevalueofthebondcalculatesouttobe$879.105.

Notethatthisbondvalueincludestheaccruedinterest.Thisisoftenreferredtoasthedirtypriceorthefullprice.Unfortunately,whenusingafinancialcalculator,youcan'tjustinputNas5.4722,sincethecalculatorwillholdthefractionalperiodtotheendratherthanconsideritupfront,andyou'llendupwiththewronganswer($863.49).Theeasiestwaytocomputethedirtypriceonyourfinancialcalculatoristoaddupthepresentvaluesofeachcashflow.

∙N=0.4722,I/Y=6,FV=30,PMT=0;CPTPV=29.18

∙N=1.4722,I/Y=6,FV=30,PMT=0;CPTPV=27.53

∙N=2.4722,I/Y=6,FV=30,PMT=0;CPTPV=25.97

∙N=3.4722,I/Y=6,FV=30,PMT=0;CPTPV=24.50

∙N=4.4722,I/Y=6,FV=30,PMT=0;CPTPV=23.12

∙N=5.4722,I/Y=6,FV=1030,PMT=0;CPTPV=748.79

∙Addeachcashflowfora879.09(roundingerror)dirtyvaluation.

Bondpricesarequotedwithouttheaccruedinterest.Thisisoftenreferredtoasthecleanprice(orjusttheprice).Todeterminethecleanprice,wemustcomputetheaccruedinterestandsubtractthisfromthedirtyprice.Theaccruedinterestisafunctionoftheaccruedinterestperiod,thenumberofdaysinthecouponperiod,andthevalueofthecoupon.Theperiodduringwhichtheinterestisearnedbytheselleristheaccruedinterestperiod.Assumeafractionalperiodof0.4722andabondpriceof$879.105.Sincethe“w”previouslycalculatedisthenumberofdays’interestearnedbythebuyerdividedbythenumberofdaysinthecouponperiod,theAIperiodisthecomplementof“w”.Hence:

AI=(1-w)*CPN

=(1–0.4722)*30=$15.833

Therefore,thecleanpriceis:

CP=dirtyprice–AI=$879.105–15.833=863.272.Thebondwouldbequotedat86.3272%(orapproximately8610/32)ofpar.

j:

Explainthedeficiencyofthetraditionalapproachtovaluationinwhicheachcashflowisdiscountedatthesamediscountrate.

Theuseofasinglediscountfactor(i.e.,YTM)tovalueallbondcashflowsassumesthatinterestratesdonotvarywithtermtomaturityofthecashflow.Inpracticethisisusuallynotthecase—interestratesexhibitatermstructure,meaningthattheyvaryaccordingtotermtomaturity.Consequently,YTMisreallyanapproximationorweightedaverageofasetofspotrates(aninterestratetodayusedtodiscountasi

- 配套讲稿:

如PPT文件的首页显示word图标,表示该PPT已包含配套word讲稿。双击word图标可打开word文档。

- 特殊限制:

部分文档作品中含有的国旗、国徽等图片,仅作为作品整体效果示例展示,禁止商用。设计者仅对作品中独创性部分享有著作权。

- 关 键 词:

- 十五 Asset Valuation Debt Investments Analysis and

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

《贝的故事》教案4.docx

《贝的故事》教案4.docx

-

《对韵歌》优秀教案8.docx

-

《函数yAsinωx+φ+P图象》wwwnet.docx

-

《静夜思》教学设计.docx

-

《汽车底盘构造与维修》题库与考核标准.docx

-

《世说新语》复习资料.docx

-

《我的服装我做主》教案设计.docx

-

《在品味情感中成长》教学片断设计.docx

-

11造价员《建设工程造价管理基础知识》精讲教程文件.docx

-

《不会叫的狗》教案 人教部编版1.docx

-

《操作系统》二学期A卷及答案.docx

-

《傅雷家书》名著阅读笔记.docx

-

《反不正当竞争法》下互联网平台封禁行为考辨以消费者用户合法权益保护为中心.docx

-

《化工原理》第六章蒸发.docx

-

《蓝海战略》概要11页.docx

-

《人生》读书心得.docx

-

《荷叶圆圆》公开课教案优秀教学设计26.docx

-

《科技出行研究报告》智能网联与新能源将变革未来汽车出行.docx

-

《272 向量的应用举例》导学案1.docx

-

《秋天》评课稿.docx

-

《电算化》第二章会计电算化的工作环境章节练习.docx

-

《室外给排水管道》施组.docx

-

《广东省建筑与装饰工程综合定额》计算规则.docx

-

《我多想去看看》教学.docx

-

《直通车车手基础认证》 考试答案 70题之欧阳育创编.docx

-

7天销量翻10倍皇冠卖家教您玩转最精准流量.docx

-

9 阿长和山海经.docx

-

《比例尺》教案.docx

-

《菜根谭》注译四闲适篇.docx

-

《福尔摩斯探案集》读后感15篇.docx

-

《红对勾》古代诗歌选择题答案补充.docx

-

《课堂密码》读后感及心得精选多篇.docx

-

电压互感器123精编版.docx

-

电子书包使用体会.docx

-

东城区初三二模化学试题及答案.docx

-

动物遗传资源保护概论.docx

-

端午节知识竞赛题.docx

-

对银行服务的感谢信五篇范文.docx

-

儿童节游乐场活动方案.docx

-

二级建造师《公路工程管理与实务》真题II卷 附答案.docx

-

二年级数学暑假作业共天.docx

-

发电部两票三制管理制度.docx

-

法语学习0Siuby上海教师资格证考试心理学测试题及答案1614 共39页word精品文档40页.docx

-

部编版六年级语文上册 21文言文二则 优秀教学设计推荐.docx

-

青岛版五四制四年级数学上册教案 全集.docx

-

热电厂利用吸收式热泵提取余热供暖方案项目可行性研究报告书.docx

-

人教版五年级数学下册约分专项练习题81.docx

-

人教版小学四年级英语上册教材分析及全册教案最新版.docx

-

人教版语文小学四年级下册全册教案2.docx

-

财经学院首届职业生涯规划策划书.docx

-

山东省滨州市惠民县学年高二上学期期末考试 英语含答案.docx

链接地址:https://www.bdocx.com/doc/28345526.html