整理SAP+FI+汇率与外币评估.docx

整理SAP+FI+汇率与外币评估.docx

- 文档编号:25902173

- 上传时间:2023-06-16

- 格式:DOCX

- 页数:24

- 大小:825.71KB

整理SAP+FI+汇率与外币评估.docx

《整理SAP+FI+汇率与外币评估.docx》由会员分享,可在线阅读,更多相关《整理SAP+FI+汇率与外币评估.docx(24页珍藏版)》请在冰豆网上搜索。

整理SAP+FI+汇率与外币评估

汇率与外币评估

汇率设置:

OC47|OB07,OB08|OC41,SE16:

V_TCURF

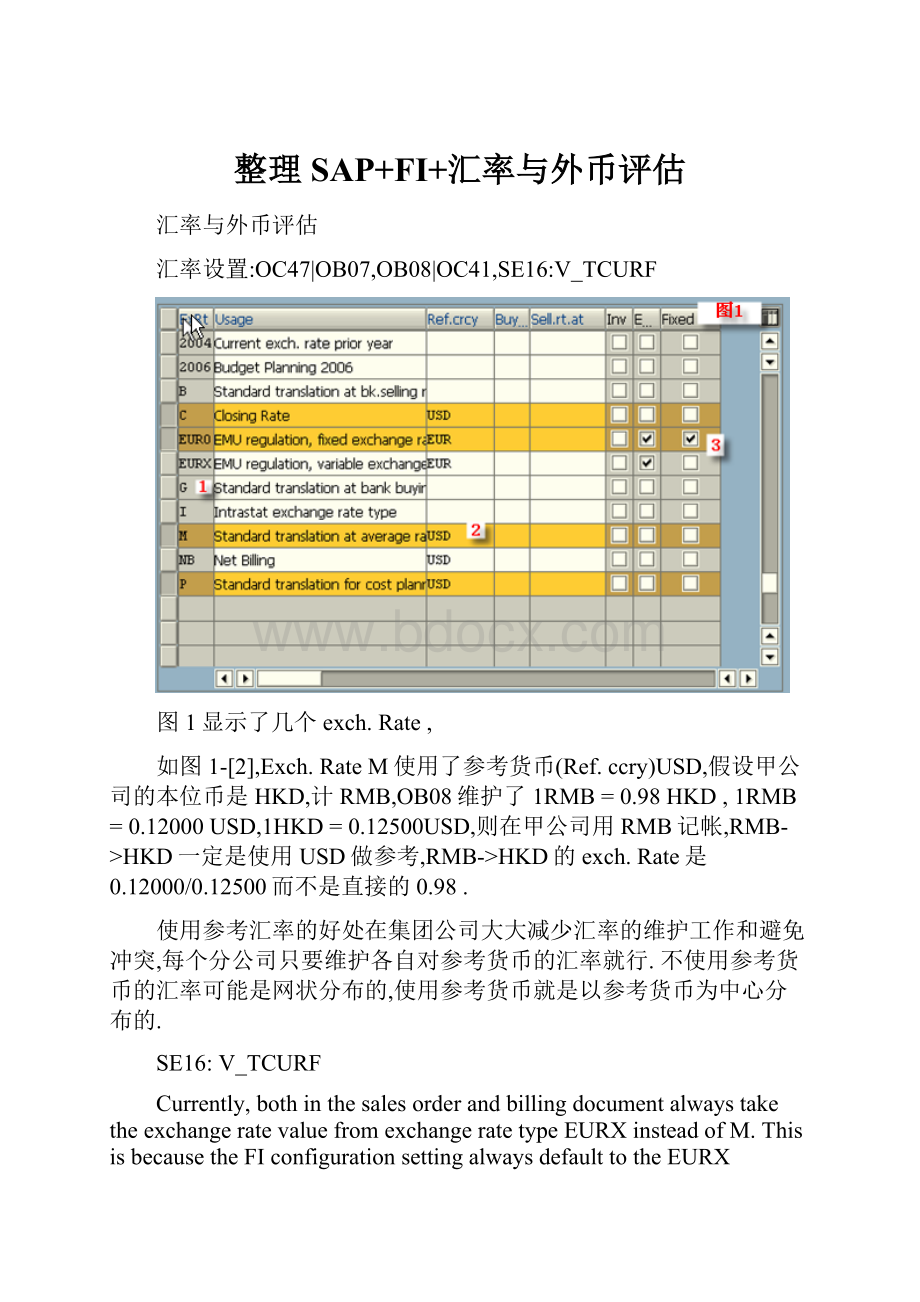

图1显示了几个exch.Rate,

如图1-[2],Exch.RateM使用了参考货币(Ref.ccry)USD,假设甲公司的本位币是HKD,计RMB,OB08维护了1RMB=0.98HKD,1RMB=0.12000USD,1HKD=0.12500USD,则在甲公司用RMB记帐,RMB->HKD一定是使用USD做参考,RMB->HKD的exch.Rate是0.12000/0.12500而不是直接的0.98.

使用参考汇率的好处在集团公司大大减少汇率的维护工作和避免冲突,每个分公司只要维护各自对参考货币的汇率就行.不使用参考货币的汇率可能是网状分布的,使用参考货币就是以参考货币为中心分布的.

SE16:

V_TCURF

Currently,bothinthesalesorderandbillingdocumentalwaystaketheexchangeratevaluefromexchangeratetypeEURXinsteadofM.ThisisbecausetheFIconfigurationsettingalwaysdefaulttotheEURXexchangeratetypeforEUR<->USD,thusitneedtobechangedsoitcantaketheratewiththeexchangeratetypeM.

Inthecurrentsetting,theEURXhasbeendefinedinthecurrencytranslationratioforexchangeratetypeM.TheEURXneedtoberemovedfromcolumn"Alt.ERT"forexchangeratetypeMforcurrencytranslationfromUSD<->EUR.

就是说不使用EURX做EUR<->USD而是使用Mexch.Ratetype,该死的Exch.RateEURX.

外币评估:

OB59,OBA1->KDF|OB09

注意Z001/Z002使用的exch.Rate是C,Z002选上了BalanceValuat.选择.

TMD这个破Balancevalut.是篾意思?

看SAP的帮助

BalanceValuationforOpenItems

Ifyouselectthisparameter,openitemsarebalancedperaccountorgroupandcurrency.Thebalanceisvaluatedaccordingtothevaluationmethod.Thevaluationdifferenceispostedasanexpenseorrevenue(peraccount,onlyrevenueORexpense).

Ifyoudonotselectthisparameter,theopenitemsaresummarizedandvaluatedperreferencenumber.Ifthereisnoreferencenumber,eachlineitemisvaluatedindividually.Thedifferencesthatarisearepostedasanexpenseorrevenue(peraccount,expenseANDrevenue).

Example:

3lineitems:

A,BandC

A Referencenumber1 100USD 190

B Referencenumber1 30-USD 50-

C Noreferencenumber 10USD 15

1)Nobalancevaluation,lowestvalueprinciple,spotexchangerate1.8

Totalfrom A+B 70USD 140DEM Valuationdifference14-DEM

(70*1.8=126 126-140=-14)

C 10USD 15DEM Novaluation,duetolowest

valueprinciple

2)Balancevaluation,lowestvalueprinciple,spotexchangerate1.8

TotalA-C 80USD 155DEM Valuationdifference=11-DEM

(80*1.8=144-155=-11)

Thetotalispostedasanexpense.

3)Nobalancevaluation,revaluationanddevaluation,spotexchange

rate1.8

TotalA+B 70USD 140DEMvaluationdifference 14-DEM

(70*1.8=126 126-140=-14)

C 10USD 15DENvaluationdifference +3DEM

Postings,expense14DEM,revenue3DEM

Z004同Z003唯一不同的是Z004的BalanceValuat.选上了,Z003和Z004是专门重置外币评估的方法

外币评估F.05通常分成2类评估

1.以外币记帐的客户/供应商/总帐未清项(D/K/S)->对所有的未清项进行评估

(余额虽为0,但有未清项)

2.以外币记帐的资产负债表科目(即科目货币非本位币)->对外币余额进行评估

确定评估差异有两种方法:

1.在资产负债表出表日确认并在下月1日冲销

2.在资产负债表出表日确认并更新被评估的未清项,不冲销

未清项的评估是在外币的汇率有变化时,对有涉及外币未清项的科目按统驭科目或科目类型、按币种、分借贷分别进行统计其由于汇率变化产生

的差额,将变化额按科目类型和币种进行帐务调整。

f-03、f-28、f-32你是在做这些记账操作的时候,item中出现valuationaccount吗?

是的,

去查出现此种情况的原会计凭证科目Openitem的moredata中均有valuationdiff金额。

外币评估简单操作.

也就是OpenItemBSEG的这个破BDIFF字段评估后有了差异(如下图).

想一个问题,为什么在F-32,F-44会有类型凭证?

把供应商与客户一起选中执行,结果只产生外币评价凭证未产生相应的回转凭证.抛账会计凭证举例如下:

DR:

F/XLOSS-Unreali*** DR:

ARrev ***

Cr:

ARrevluation*** Cr:

F/Xgain-Unreali***

现在在做冲账动作时,只要产生汇兑损益情况,均会抛出外币评价科目.举例如下:

借:

银行存款 100HKD 112RMB

贷:

应收账款-XXX 100HKD 112RMB

借:

汇兑损失 0HKD xxRMB

贷:

应收账款外币评价0HKD xxRMB

FI-IncorrectExchangeRatedeterminationinForeignCurrencyValuationinF.05

TheEuroLoanisvaluatedmonthlyinCCcurrencyaswellasGroupCurrency.ThedifferencedenotedtheforeignExchangeGain/Lossuponvaluation.TheGLA/c30010010wasvaluedforthisloanon29/01/05.Butthedifferenceappearstobetoohigh.

wondertheformulainstep1whichistorevaluateforeigncurrencytoclosingmonthendrateisnotright.Inmeasuring10MEUR,howcomestep1saysUS$11Mlosswhilestep2saysUS$10Mgain?

Pleaseinvestigate.

ItisnecessarytoinvestigateandclosethisissueASAPasmonthlyclosingisheldupforthis.

F.05

EstimatedMan-day

IfwehaveacloselookatGL30010010forCC5100wefindthatanumberofentrieshavebeenpostedonabackdate.Pls.seetheworksheetbelow.

NowwhentheTransactionF.05wascarriedouton03/21/2005,thepositionoftheGLwasthatTheEURvaluewas10M

EUR,thelocalCurrencyvaluewasalso10MHKDwhiletheUSDvaluewas12,223,092.47allincredit.Atthispoint,the

systemtriedtovaluate10MEUROintoHKDasstep1.ItfoundtheexchangeratefromEURtoHKDusingUSDas

referencecurrencytobe10.16381.Thusthevaluationcameto101.638MHKD.Thebalanceinbookswas10M.soit

postedadifferenceof91.638Mincreditsignifyinganactualliabilityof101.638Mintotal(Documentno.600002097).While

itvaluatedinHKD,italsocarriedoutavaluationinGroupcurrencywhichwasasimpleconversionofHKDtoUSDatthe

Crateexistingonthatdate1HKD=0.12820USD.i.e.HKD91,638,065.52HKD*0.12820=11,748,000.00.Thisitpostedas

aliability.SonowthetotalliabilityinUSDcameto11,748,000.00+originalliability12,223,092.47=23,971,092.47USDor

23.971M.

Sowhenittriedtodoagroupvaluationinstep2itfoundtheactualliabilitytobe10,000,000EUR*1.30300(Exchange

ratefor1EURto1USD)=

13,030,000or13.030MUSD.ButtheGLvaluewas23,971,092.47USD.Soitpostedadebitof23,971,092.47-13,030,000=

10,941,092.47or10.941

MUSD.

Fromthesystempointofviewthereisnomistake.ItcalculatedvaluesasperBalancesexistinginthesystemonaparticular

date.

HencethevariationinGain/LossAccount.

FIChangeF.05Step1andStep2variants

CurrentlyeachentitiesusesthefollowingvariantswhenrunningF.05

/XXXX_STEP1and/XXXX_STEP2whereXXXXisreplacedbytheapplicablecompanycode.

ThesevariantsareprotectedsothattheycanonlybechangedbyuserDANIELLEB.

GlennhasrequestedthatGLaccountsbeginningwith14and20beexcludedfromthevariants.AdditionallytheseGLaccountsshouldberemovedfromtheconfiguraitonwhichisusedinF.05(thiswouldpreventthemfromeverbeingvaluated).

Attachedistheexistingsetupforboth/XXXX_STEP1and/XXXX_STEP2

FIChangeF.05Step1andStep2variants

CurrentlyeachentitiesusesthefollowingvariantswhenrunningF.05

/XXXX_STEP1and/XXXX_STEP2whereXXXXisreplacedbytheapplicablecompanycode.

ThesevariantsareprotectedsothattheycanonlybechangedbyuserDANIELLEB.

GlennhasrequestedthatGLaccountsbeginningwith14and20beexcludedfromthevariants.AdditionallytheseGLaccountsshouldberemovedfromtheconfiguraitonwhichisusedinF.05(thiswouldpreventthemfromeverbeingvaluated).

Attachedistheexistingsetupforboth/XXXX_STEP1and/XXXX_STEP2

F.05的简单操作

1.运行OB08,输入月末汇率

2.运行F.05输入参数如下图所示:

3.这里我选择的是一个客户,真正运行时可以选择客户,供应商,总帐科目,根据评估需要进行选择。

4.执行后如下图所示

5.点击按钮“posting”产生如下图画面

6.运行SM35,可以看到刚刚生成的一个会话

7.执行此会话,如下图选择参数。

8.执行过程中如出现错误,在线更改,或者中止,修改错误后再执行。

不会出现严重错误,因为此会话只是做凭证记账,会计凭证过账常见的错误你们都可以处理的。

为什么清帐时clearingdate被更改了

Issue:

WhileperformingF-32|FB1Dforcustomeropenitemclearing,forexample,wemightcleartheinter-companycustomeropenitemswithUSD(localcurrencyofcompanycode5100isHKD)on02/27/2006,however,wewanttocleartheOIonthepreviousperiod,soweinput02/18/2006.

Thentheissueoccurs,thepostingdateis02/18/2006whiletheclearingdateis02/27/2006.

Then,ifweuseFBL5Ntodisplaycleareditemswithclearingdate,actuallythedataisinconsequent.

ReasonInvestigation

Keywords:

Partialpayment|ResidualPayment

(1)Tcode:

F-32orFB1D

Forexample,ifwechoosepartialpmt,

Thereare3docwithpostingdate02/23/2006,02/18/2006and02/15/2006.

Weusethedocumentpostedin02/23/2006toclearthe2docspostedin02/18/2006and02/15/2006.

Icheckedtheprogram,andfindfinallytheother2docswillusetheclearingdoc’spostingdate02/23/2006asclearingdate.

This’sthegenerateddocument,sincethedocument5100000023postedin02/23/2006hasremainingamount,itisnotaclearingitems.

2.环境价值的度量——最大支付意愿

WithFBL5N,wehavetoinputclearingdate02/23/2006forcleareditemsearch.

二、环境影响评价的要求和内容

(1)规划实施后实际产生的环境影响与环境影响评价文件预测可能产生的环境影响之间的比较分析和评估;

仍以森林为例,营养循环、水域保护、减少空气污染、小气候调节等都属于间接使用价值的范畴。

SAPonlinehelp

(3)评价单元划分应考虑安全预评价的特点,以自然条件、基本工艺条件、危险、有害因素分布及状况便于实施评价为原则进行。

ClearingDate

(3)机会成本法Theclearingdatespecifiesasfromwhentheitemistoberegardedascleared.Whenclearing,thelastpostingdateofallthedocumentsinvolvedinclearingissetastheclearingdate.

Examples

专项规划中的指导性规划 环境影响篇章或说明Invoiceswhichwerepostedon10/10/1997andon10/15/1997areclearedbyapaymentdocumentwhichispostedon11/10/1997.Inthiscasetheclearingdateis11/10/1997,inotherwordsthepostingdateofthepaymentdocument.

1.依法评价原则;ArentalinvoiceforDecemberisenteredon11/28/1997andthepostingdateissetto12/01/1997.Therentispaidon11/30/1997andisalsopostedunderthisdate.12/01/1997isthensetastheclearingdate,inotherwordsthepostingdateoftheinvoice.

Dependencies

Theclearingdateofalineitemisneverallowedtobebeforethepostingdateoftheitem.

Eg.Onlyforpayment,theclearingdateispaymentdate.

(5)阐述划分评价单元的原则、分析过程等。

规划审批机关在审批专项规划草案时,应当将环境影响报告书结论以及审查意见作为决策的重要依据。

一.外币未清项评估原理

1.外币的未清项评估适用范围

1)应收帐款。

2)其他往来应收。

3)应付帐款。

4)应付工资。

5)其他应付。

6)预提费用。

7)借款。

2.原理。

未清项的评估是在外币的汇率有变化时,对有涉及外币未清项的科目按统驭科目或科目类型、按币种、分借贷分别进行统计其由于汇率变化产生的差额,

- 配套讲稿:

如PPT文件的首页显示word图标,表示该PPT已包含配套word讲稿。双击word图标可打开word文档。

- 特殊限制:

部分文档作品中含有的国旗、国徽等图片,仅作为作品整体效果示例展示,禁止商用。设计者仅对作品中独创性部分享有著作权。

- 关 键 词:

- 整理 SAP FI 汇率 外币 评估

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

《 岁婴幼儿教养方案》.docx

《 岁婴幼儿教养方案》.docx

-

《分数混合运算》导学案模板.docx

-

《管理学概论》案例分析作业48122第8组.docx

-

《全职高手》手游每日答题答案162题.docx

-

《手影游戏》教案.docx

-

《夏洛的网》读书笔记15篇.docx

-

《《宝莱坞生死恋》观后感》.docx

-

《父亲的病》读后感.docx

-

《仙人掌》大班教案.docx

-

《浙江省建筑业企业资质管理实施办法》.docx

-

1一年级看图写话图片.docx

-

3汽车整车气动声学风洞风噪试验车内风噪测量方法0330报批稿1.docx

-

《北师大资深教授顾明远做主题发言》.docx

-

《第27届飞天奖颁奖词》.docx

-

《悲惨世界》读书心得范文.docx

-

《登革热演练方案》.docx

-

《怀孕40周每周详解》最新完整版.docx

-

《建设工程施工管理》真题及答案.docx

-

《雷雨》教案1.docx

-

《模具制造工》培训大纲.docx

-

《社区医疗活动方案》.docx

-

《首届诺贝尔奖颁发》教案.docx

-

《移动通信技术》实验教学大纲186教学文案.docx

-

1纤维的种类特性性能.docx

-

3口腔执业医师综合笔试习题.docx

-

4章制药习地训练题目.docx

-

8中医养生保健技术规范穴位贴敷.docx

-

20种空调常见故障判断与维修.docx

-

201X年暑假机关会计社会实践报告.docx

-

500td光伏污水处理改造工程设计方案.docx

-

APP管理端概述说明.docx

-

《保护心脏》第二课时教学设计.docx

-

级大学生职业发展与就业指导答案精Word文档下载推荐.docx

-

加油站ppt工作汇报Word文件下载.docx

-

教师考试教育法律法规试题汇总及答案7Word文档格式.docx

-

胡志远老师作文讲座摘抄Word格式文档下载.docx

-

监狱生活卫生安全管理问题初探Word格式文档下载.docx

-

三年级上册科学专项练习题大全Word文件下载.docx

-

届高考历史热点专题2 精品推荐Word下载.docx

-

年产吨核桃加工制品车间建设项目可行性报告Word文件下载.docx

-

金融保险存款保险制度及其利弊分析Word文件下载.docx

-

交管培养方案Word文档下载推荐.docx

-

建筑工程施工总承包合同Word格式.docx

-

家庭工程施工合同范本Word格式.docx

-

科技企业可持续发展能力的财务分析以东软集团为例Word文件下载.docx

-

人脸定位算法研究文档格式.docx

-

七年级下册地理重点湖南教育出版社Word格式文档下载.docx

-

垃圾渗滤液设计方案Word文档格式.docx

-

建筑施工安全检查标准Word格式.docx

-

洁净区容器具清洁消毒标准操作规程定稿Word文件下载.docx

-

建设工程合同管理毕业论文文档格式.docx