FRMExam完整版真题试题.docx

FRMExam完整版真题试题.docx

- 文档编号:23361463

- 上传时间:2023-05-16

- 格式:DOCX

- 页数:69

- 大小:77.34KB

FRMExam完整版真题试题.docx

《FRMExam完整版真题试题.docx》由会员分享,可在线阅读,更多相关《FRMExam完整版真题试题.docx(69页珍藏版)》请在冰豆网上搜索。

FRMExam完整版真题试题

Question1

Whichtypeofoptionproducesdiscontinuouspayoffprofiles.meaningthatthepayoffdoesnotincreaseordecreasecontinuouslywiththeunderlyingassetvalue?

a.Chooseroptions

b.Barrieroptions

c.Binaryoptions

d.Lookbackoptions

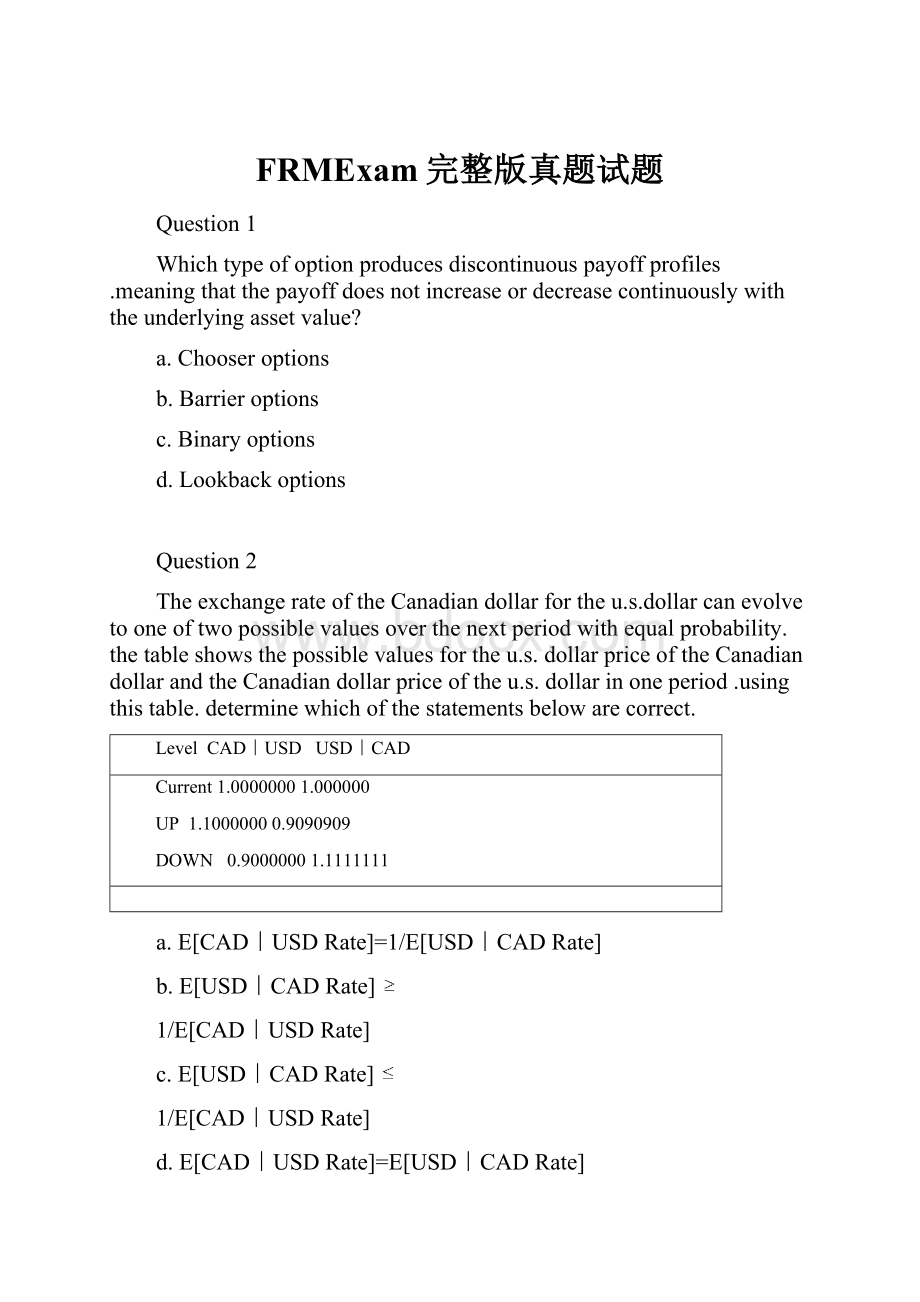

Question2

TheexchangerateoftheCanadiandollarfortheu.s.dollarcanevolvetooneoftwopossiblevaluesoverthenextperiodwithequalprobability.thetableshowsthepossiblevaluesfortheu.s.dollarpriceoftheCanadiandollarandtheCanadiandollarpriceoftheu.s.dollarinoneperiod.usingthistable.determinewhichofthestatementsbelowarecorrect.

LevelCAD|USDUSD|CAD

Current1.00000001.000000

UP1.10000000.9090909

DOWN0.90000001.1111111

a.E[CAD|USDRate]=1/E[USD|CADRate]

b.E[USD|CADRate]

1/E[CAD|USDRate]

c.E[USD|CADRate]

1/E[CAD|USDRate]

d.E[CAD|USDRate]=E[USD|CADRate]

Answerquestions3and4basedonthefollowinginformation

AriskmanagerforABCbankhascompiledthefollowingdateregardingabondtraderandanequitytrader.Assumethatthereturnsarenormallydistributedandthatthereare52tradingweeksperyear.ABCbankcomputesitscapitalusinga99%VaR.theafter-taxprofitsareall-inclusive.

ABCBankDate—USDmillions

After-taxnetbookweeklytax

Profitmarketvaluevolatilityrate

Bondtrader

Equitytrader

USD8USD1201.1%40%

USD18USD1801.94%40%

Question3

UsingtheABCbankdate.calculatetheannualrisk-adjustedreturnoncapital(RAROC)forthebondtrader?

a.25.24%

b.36.08%

c.60.15%

d.84.92%

Question4

UsingtheABCbankdate.whichofthefollowingstatementsarecorrectinrelationtotheequitytrader?

Theequitytraderhasanannual.after-taxVaRata99%confidoncelevelofUSD33.2million.

IncomparingtheRAROCforbothtraders.theequitytraderisperformingbetterthanthebondtrader.

a.Ⅰonly

b.Ⅱonly

c.Both

d.Neither

Question5

Thestand-aloneeconomiccapitalrequirementsforinsurancecompaniescanbebrokendownintothreemajorrisk;creditrisk,market/ALMriskandoperatingandotherrisks.analyzingtherisk.profilesofalifeinsurer;aP&Cinsurer.Adiversifiedinsurer,andapropertyinsurerthehighestmarket/ALMriskwouldbefora:

a.Lifeinsurer

b.P&Cinsurer

c.Diversifiedinsurer

d.Propertyinsurer

Question6

companyXYZ’spensionfundhasliabilitiesofUSD100millionandassetsofUSD120million.Theannualgrowthoftheliabilitieshasanexpectedvalueof5%with3%volatility.thereturnoftheassetshasanexpectedvalueof8%with12%volatility.Thecorrelationbetweenassetreturnandliabilitygrowthis0.3.whatisthe95%surplus-at-risk?

a.USD27.6million

b.USD22.7million

c.USD13.8million

d.USD18.1million

Question7

consideranall-equityfirmwithequitycapitalizationofUSD2billion.Thefirm’sCFOconsidersthefollowingthreefinancingstrategies

1.issuezero-couponseniordebtwithprincipalamountofUSD1billionpayablein10yearsandpurchaseinsuranceforUSD100millionthatwillpaylossesontheseniordebttoinvestorsinexcessofUSD500million

2.issuezero-couponjuniordebtwithprincipalamountofUSD500millionpayables10yearsandissuezero-couponseniordebtwithprincipalamountofUSD500millionpayables10years

3.issuezero-couponseniordebtwithprincipalamountofUSD1billionpayable10yearswithaputoptionattachedthatgivesinvestorstherighttoputdebttothefirmatmaturityfortheprincipalamount

whichofthesesstrategieswouldhavethemostriskyseniordebt?

a.Strategy1

b.Strategy2

c.Strategy3

d.Seniordebtsareequallyriskyinallthreestrategies

Question8

gammaindustriesincissuesaninversefloaterwithafacevalueofUSD50.000.000thatpaysasemiannualcouponof1150%minusLIBROgammaindustriesintendstoexecuteanarbitragestrategyandearnaprofitbysellingthenotes.Usingtheproceedstopurchaseabondwithafixedsemiannualcouponrateof6.75%ayearandthenhedgetheriskbyenteringintoanappropriateswap.Gammaindustriesreceivesaquotefromaswapdealerwithafixedrateof5.75%andafloatingrateofLIBOR.WhatwouldbethemostappropriatetypeofswapofGammaindustries,Inc.,toenterintotohedgeitsrisk?

a.Pay-fixed,receive-fixedswap

b.Pay-floating,receive-fixedswap

c.Pay-fixed,receive-floatingswap

d.Theriskcannotbehedgedwithaswap

Question9

aportfoliomanagerentersintoatotalofreturnswapasthetotalreturnreceiver.Underwhichofthefollowingsituationswouldtheportfoliomangerberequiredtomakeanetoutlaytothecounterparty?

a.Ifthetransactionwasinitiatedasahedge.Thennooutlaywasrequired

b.Iftherewereacapitalgainonthereferenceasset

c.Ifthemarketvalueofthereferenceassetdecreasedsignificantly

d.Ifthespreadbetweenthereferenceassetandthebenchmarkassetchanged

Question10

whichofthefollowingstatementsaboutcombatingmodelriskareincorrect?

1Ifapositionisknowtohaveconsiderablemodelrisk.Afirmcanlimititsexposurebyimposingatighterpositionlimit

2Ifwealwayschoosethemodelthattakesintoaccountthelargestnumberofreal-worldfactorsthataffectprices.Thefirm’sexposuretomodelriskwillbereduced

3Runningregularstresstestsorscenarioanalysestotestthevolatility.Correlationandliquidityassumptionsinmodelhelpsreducemodelrisk

4Riskmanagersshouldcheckthetrader’spricingmodeltoensurethatmodelcalibrationisup-to-dateandthatmodelsareupgradedinlinewithmarketbestpracticeandtoensurethatobsoletemodelsareidentifiedandtakenoutofuse

a.Nonearetrue

b.Ⅱonly

c.Ⅰ,ⅢandⅣ

d.Ⅰ,ⅡandⅢ

Question11

Whichtypeofdistributionproducesthelowestprobabilityforavariabletoexceedaspecifiedextremevalue“X”Whichisgreaterthanthemean,assumingthedistributionallhavethesamemeanandvariance?

a.Aleptokurticdistributionwithakurtosisof4.

b.Aleptokurticdistributionwithakurtosisof8.

c.Anormaldistribution.

d.Aplatykurticdistribution.

Question12

AnAmericaninvestorholdsaportfolioofFrenchstocks.Themarketvalueofportfoliois€10million,withabetaof1.35relativetoCACindex.InNovember,thespotvalueoftheCACindexis4750.TheexchangerateisUSD1.25/€.Thedividendyield.aurointerestratesanddollarinterestratesareallequalto4%.Whichofthefollowingoptionstrategieswouldbethemostappropriatetoprotecttheportfolioagainstadeclineoftheeuro?

MarchEurooptions(allpricesinUSdollarper€)

StrikeCalleuroPuteuro

1.250.0180.022

a.BuycallswithapremiumofUSD160,000.

b.BuyputswithapremiumofUSD220,000.

c.SellcallswithapremiumofUSD180,000.

d.SellputswithapremiumofUSD220,000.

Question13

Inanattempttoprovideguidanceonanadditionalstepstobetakenbytheprivatesectortopromotetheefficiency,effectivenessandstabilityoftheglobalfinancialsystem.ThecounterpartyriskmanagementpolicyGroupII(GRMPGII)publishedareportinJuly2005containingrecommendationsandguidingprinciples.AccordingtotheGRMPGIIreport,whichofthefollowingstatementsrelatingtoEmergingIssueisincorrect?

a.GRMPGIIrecommendsthatfiduciariestakingonrisksassociatedwithcomplexproductsshouldhavetheabilitytoaggregateriskacrosstheirentirepoolofassetsinordertounderstandportfolio-levelimplications.

b.GRMPGIIrecommendsthathedgefunds.onavoluntarybasis,adopttherelevantrecommendationsandguidingprinciplescontainedintheir(GRMPGII)report.

c.Asaguidingprincipleinsellingstructuredproductstoretailinvestors,financialintermediariesshouldconsiderwhetherdisclosureappropriatelyconveysthefactthatsecondarymarketvalue,atmaturity,willbelessthantheissueprice.

d.Asaguidingprinciple,seniormanagementshouldconductperiodicreviewsofthefinancialintermediary’sinternalcontrolsforthesaleofcomplexproductsretailinvestors.

Question14

Whichstatementbestdescribescorrelationsanvariancesintimesoffinancialcrisis?

a.Thereareonlymarginalchangesincorrelationsandvariancesintimesofcrisis,andthereforetheydonotneedtobefactoredintoriskmanagement.

b.Thediversificationbenefitsdecreasebecausecorrelationsincrease,andthereforeyourrisklevelincreases.

c.Thediversificationbenefitsincreasebecausecorrelationsdecrease,andthereforeyourriskleveldecreases.

d.VaRestimatesusingtheRiskmetricsapproachprovidefortheeffectsofincreasedcorrelationsduringperiodscrisis,andthereforetheeffectsarefactoredintocurrentpositions.

Question15

Assumethemarginalmonthlydefaultrates(conditionalonnopreviousdefault)forafirmare2%eachmonthduringthefirstyearand3%eachmonthduringthesecondyear.Whatisthemarginalprobabilityofdefaultingoverthethesecondyear,conditionalonnothavingdefaultedthefirstyear?

a.Insufficientinformationtoanswerthequestion

b.30.6%

c.36.0%

d.47.4%

Question16

GiventworandomvariablesXandY,WhatisthevarianceofX,GivenVariance[Y]=100.

Variance[4X-3Y]=2,700andthecorrelationbetweenXandYis0.5?

a.56.3

b.113.3

c.159.9

d.225.0

Question17

Aportfoliohasanaveragereturnoverthelastyearof13.2%.Itsbenchmarkhasprovidedanaveragereturnoverthesameperiodof12.3%.Theportfolio’sstandarddeviationis15.3%,itsbetais1.15,itstrackingerrorvolatilityis6.5%anditssemi-standarddeviationis94%.Lastly,therisk-freerateis4.5%.Calculatetheportfolio’sinformationRatio(IR).

a.0.569

b.0.076

c.0.138

d.

- 配套讲稿:

如PPT文件的首页显示word图标,表示该PPT已包含配套word讲稿。双击word图标可打开word文档。

- 特殊限制:

部分文档作品中含有的国旗、国徽等图片,仅作为作品整体效果示例展示,禁止商用。设计者仅对作品中独创性部分享有著作权。

- 关 键 词:

- FRMExam 完整版 试题

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

《化学反应的快慢和限度》教案鲁科版必修2.docx

《化学反应的快慢和限度》教案鲁科版必修2.docx

-

《21世纪大学实用英语》综合教程课程教学大纲.docx

-

《赶海》的教学设计.docx

-

《小儿推拿如何治感冒》教学设计方案.docx

-

《每个孩子都能成功》读后感1000字.docx

-

1 我们的远古祖先.docx

-

《试吧大考卷》高中全程训练计划历史月考仿真一.docx

-

《统计学》试题C.docx

-

3消防安全重点单位四个能力自我评估报告备案表.docx

-

《电子商务基础与应用》慕课版配套教学教案.docx

-

《环境工程学》课程教学大纲.docx

-

《理想国》读书笔记1500字精选多篇.docx

-

《社会保险法》知识问答.docx

-

《铁路电力管理规则》《铁路电力安全工作规程》课件.docx

-

《中小学公共安全教育读本》教案.docx

-

8法律专项银行招聘考试法律法规必读知识点15页可直接打印.docx

-

10万吨年乙苯脱氢制苯乙烯装置工艺设计与实现可行性方案.docx

-

15MW风电机组运行维护手册.docx

-

20XX工作计划范文车间.docx

-

73新课程结构的主要内容与特征.docx

-

1000吨果品气调库建设项目可行性研究报告.docx

-

《8成语故事》导学案.docx

-

《分享的快乐方案》教学设计.docx

-

《建筑企业管理学》复习题及答案.docx

-

《宿舍信息管理系统》需求分析说明书.docx

-

《众筹合伙协议》合同干净版.docx

-

5以内加减法口算天天练强烈推荐110.docx

-

8年级上科学知识点总结.docx

-

10以内加减法练习题.docx

-

20XX机关效能建设工作计划.docx

-

49中学生物竞赛辅导第六章动物生理上.docx

-

081 除灰系统设备管道安装.docx

-

精品初中中考 语文 修改病句专项训练及答案Word格式文档下载.docx

-

经营企业的十二条准则Word下载.docx

-

科研个人工作总结Word文档格式.docx

-

经济效益审计课后练习题答案及案例分析思路文档格式.docx

-

经济法学多项选择题Word文档格式.docx

-

军训动员会教师发言稿docWord文档下载推荐.docx

-

临街防坠落措施Word文档下载推荐.docx

-

井冈山旅游景点导游词5篇Word文档格式.docx

-

离婚协议书有车范文2篇Word格式.docx

-

教科版科学五年级上册期末试题Word文档下载推荐.docx

-

届高三生物精准培优专练二十食物链网中能量流动含解Word文档格式.docx

-

历年广西来宾市数学中考真题及答案Word格式文档下载.docx

-

教科版五年级科学下册第一单元教学设计docxWord下载.docx

-

月度大会主持词开头范例.docx

-

科室护理质控年终总结Word下载.docx

-

江苏省南通市学年三年级第一学期期初调研数学试题含答案和解析09Word格式.docx

-

精功铸锭炉安全操作规程文档格式.docx

-

建筑工程专科实习报告Word格式文档下载.docx

-

教师岗位目标管理责任制Word文档格式.docx