亨格瑞管理会计英文第15版练习答案06.doc

亨格瑞管理会计英文第15版练习答案06.doc

- 文档编号:145261

- 上传时间:2022-10-04

- 格式:DOC

- 页数:50

- 大小:268KB

亨格瑞管理会计英文第15版练习答案06.doc

《亨格瑞管理会计英文第15版练习答案06.doc》由会员分享,可在线阅读,更多相关《亨格瑞管理会计英文第15版练习答案06.doc(50页珍藏版)》请在冰豆网上搜索。

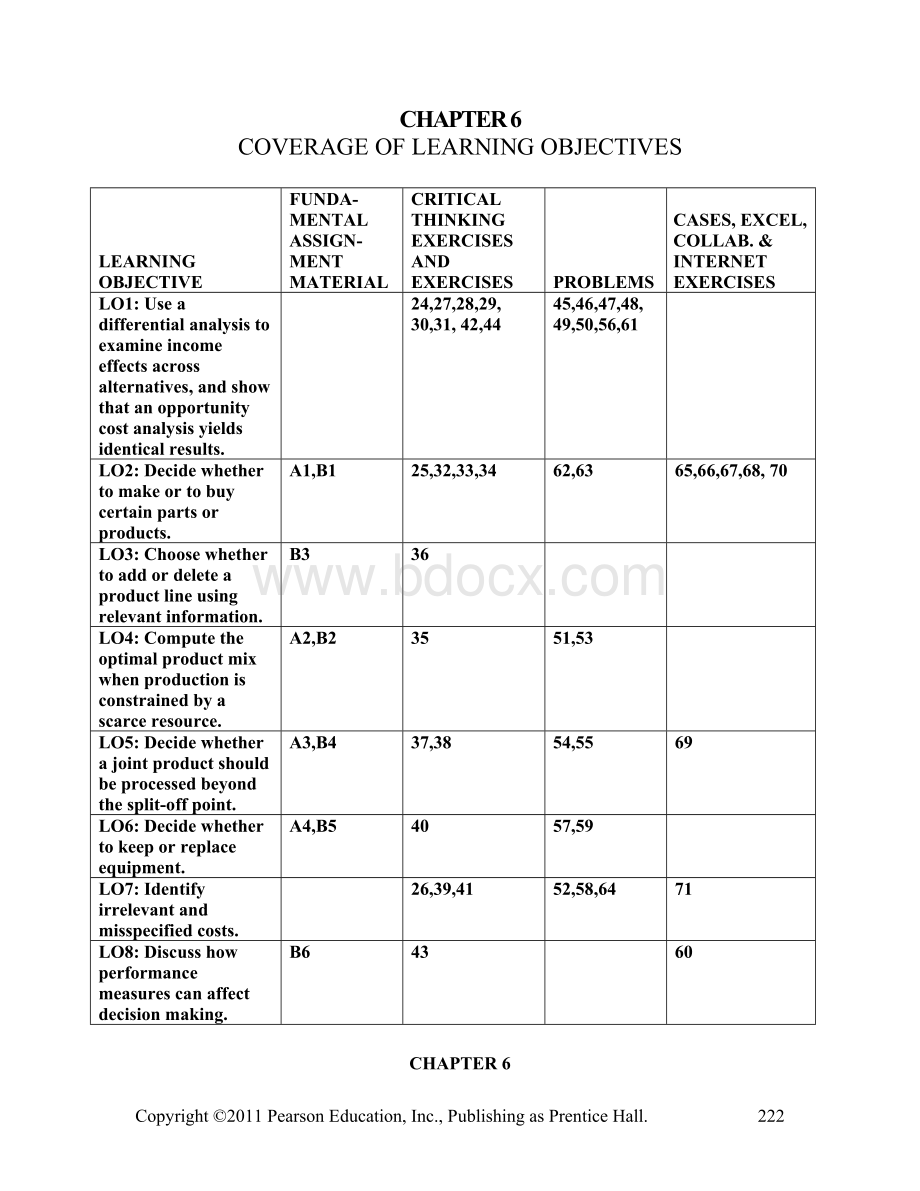

CHAPTER6

COVERAGEOFLEARNINGOBJECTIVES

LEARNINGOBJECTIVE

FUNDA-

MENTALASSIGN-MENT

MATERIAL

CRITICALTHINKINGEXERCISESANDEXERCISES

PROBLEMS

CASES,EXCEL,COLLAB.&INTERNETEXERCISES

LO1:

Useadifferentialanalysistoexamineincomeeffectsacrossalternatives,andshowthatanopportunitycostanalysisyieldsidenticalresults.

24,27,28,29,30,31,42,44

45,46,47,48,

49,50,56,61

LO2:

Decidewhethertomakeortobuycertainpartsorproducts.

A1,B1

25,32,33,34

62,63

65,66,67,68,70

LO3:

Choosewhethertoaddordeleteaproductlineusingrelevantinformation.

B3

36

LO4:

Computetheoptimalproductmixwhenproductionisconstrainedbyascarceresource.

A2,B2

35

51,53

LO5:

Decidewhetherajointproductshouldbeprocessedbeyondthesplit-offpoint.

A3,B4

37,38

54,55

69

LO6:

Decidewhethertokeeporreplaceequipment.

A4,B5

40

57,59

LO7:

Identifyirrelevantandmisspecifiedcosts.

26,39,41

52,58,64

71

LO8:

Discusshowperformancemeasurescanaffectdecisionmaking.

B6

43

60

CHAPTER6

RelevantInformationandDecisionMakingWithaFocusonOperationalDecisions

6-A1 (20min)

1. Thekeytothisquestioniswhatwillhappentothefixedoverheadcostsifproductionoftheboxesisdiscontinued.Assumethatall$60,000offixedcostswillcontinue.Then,SunshineStatewilllose$20,000bypurchasingtheboxesfromWeyerhaeuser:

PaymenttoWeyerhaeuser,80,000×$2.10 $168,000

Costssaved,variablecosts 148,000

Additionalcosts $20,000

2. Somesubjectivefactorsare:

· MightWeyerhaeuserraisepricesifSunshineStatecloseddownitsbox-makingfacility?

· Willsub-contractingtheboxproductionaffectthequalityoftheboxes?

· Isatimelysupplyofboxesassured,evenifthenumberneededchanges?

· DoesSunshineStatesacrificeproprietaryinformationwhendisclosingtheboxspecificationstoWeyerhaeuser?

3. Inthiscasethefixedcostsarerelevant.However,itisnotthedepreciationontheoldequipmentthatisrelevant.Itisthecostofthenewequipment.Annualcostsavingsbynotproducingtheboxesnowwillbe:

Variablecosts $148,000

Investmentavoided(annualized) 80,000

Totalsaved $228,000

ThepaymenttoWeyerhaeuseris$228,000-$168,000=$60,000lessthanthesavings,soSunshineStatewouldbe$60,000betteroffsubcontractingtheproductionoftheboxes.

6-A2 (10min.)

1. Contributionmargins:

Plain=$70-$55=$15

Professional=$100-$75=$25

Contributionmarginratios:

Plain=$15÷$70=21.4%

Professional=$25÷$100=25%

2. PlainProfessional

a. Unitsperhour 2 1

b. Contributionmarginperunit $15 $25

Contributionmarginperhour $30 $25

Totalcontributionfor20,000hours $600,000 $500,000

3. Theplaincircularsawsarethebestuseofthescarcemachinehours.Foragivencapacity,thecriterionformaximizingprofitsistoobtainthegreatestpossiblecontributiontoprofitforeachunitofthelimitingorscarcefactor.Moreover,fixedcostsareirrelevantunlesstheirtotalisaffectedbythechoiceofproducts.

6-A3 (15min.)Tableisinthousandsofdollars.

1,2. (a) (b) (a)-(b) (c) (a)-(b)-(c)

Separable

Sales Sales Costs Incremental

Beyond at Incremental Beyond Gainor

Split-Off Split-Off Sales Split-Off (Loss)

A 230 54 176 190 (14)

B 330 32 298 300

(2)

C 175 54 121 100 21

IncreaseinoveralloperatingincomefromfurtherprocessingofA,B,andC 5

TheincrementalanalysisindicatesthatProductCshouldbeprocessedfurther,butProductsAandBshouldbesoldatsplit-off.Theoveralloperatingincomewouldbe$44,000,asfollows:

Sales:

$54,000+$32,000+$175,000 $261,000

Jointcostofgoodssold $117,000

Separablecostofgoodssold 100,000 217,000

Operatingincome $44,000

Comparethiswiththepresentoperatingincomeof$28,000.Thatis,$230,000+$330,000+$175,000-($190,000+$300,000+$100,000+$117,000)=$28,000.Theextra$16,000ofoperatingincomecomesfromeliminatingthe$16,000lossresultingfromprocessingProductsAandBbeyondthesplit-offpoint.

6-A4 (30-40min.)

Problem6-60isanextensionofthisproblem.Thetwoproblemsmakeagoodcombination.

1. Operatinginflowsforeachyear,oldmachine:

$910,000-($810,000+$60,000) $40,000

Operatinginflowsforeachyear,newmachine:

$910,000-($810,000+$22,000*) $78,000

*$60,000-$38,000

Cashflowstatements(inthousandsofdollars):

Keep Replace

Three Three

Year Years Years Year Years Years

1 2&3 Together 1 2&3 Together

Receipts,inflowsfromoperations 40 40 120 78 78 234

Disbursements:

Purchaseof"old"equipment (90)* -- (90) (90) -- (90)

Purchaseof"new"equipment:

Totalcostslessproceeds

fromdisposalof"old"

equipment($99,000-$15,000) -- --

- 配套讲稿:

如PPT文件的首页显示word图标,表示该PPT已包含配套word讲稿。双击word图标可打开word文档。

- 特殊限制:

部分文档作品中含有的国旗、国徽等图片,仅作为作品整体效果示例展示,禁止商用。设计者仅对作品中独创性部分享有著作权。

- 关 键 词:

- 亨格瑞 管理 会计 英文 15 练习 答案 06

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

(完整word版)信息论与编码期末考试题----学生复习用.doc

(完整word版)信息论与编码期末考试题----学生复习用.doc

-

(完整)六年级上册几何图形题.docx

-

(完整)储罐防腐施工方案.doc

-

(完整word版)公务员录用体检表.doc

-

(完整)八年级上册几何证明题专项练习.doc

-

(决策管理)投资决策委员会实施细则.doc

-

(完整)四年级上册口算、竖式计算、脱式计算.doc

-

(压轴题)初中物理八年级上册第一章《机械运动》检测(含答案解析)(2).doc

-

(完整)小学三年级心理健康教案.doc

-

(完整)初中文言文翻译技巧.doc

-

(名师整理)语文中考《骆驼祥子》名著导读优秀教案.docx

-

(完整word版)偏旁部首名称大全.doc

-

(人教PEP)五年级英语竞赛试题及答案.doc

-

(完整)山东省普通高中学生综合素质评价信息管理系统操作手册学生用户手册.doc

-

(完整word版)体育课教案模板.doc

-

(住宅楼方案)房屋建筑学课程设计说明书.doc

-

(完整word版)《分数的意义》优秀教学设计(公开课).doc

-

(完整word版)安全生产标准化实施方案.doc

-

(完整)初中生人物形象分析常用词汇.doc

-

(完整版)借用公司资质协议.doc

-

(完整word版)仙剑奇侠传三图文攻略(最详细版).doc

-

(完整word版)历年陕西省专升本英语真题(答案解析超全).doc

-

(完整)四年级四则混合运算训练题100道.doc

-

(完整word版)学校团总支部换届选举方案.doc

-

(完整word版)安全标准化绩效评定计划.doc

-

(完整)分布式光伏发电项目施工组织设计.doc

-

(完整版)埋地塑料管结构环刚度计算.doc

-

(完整版)国家农业产业强镇示范建设实施方案.doc

-

(完整版)八年级数学上几何典型试题及答案.doc

-

(完整版)六年级音乐下册人音版理论知识梳理.doc

-

(完整版)囚徒健身图文教程和计划表(完美打印版).doc

(完整版)固定资产盘点表.xls

(完整版)固定资产盘点表.xls

-

XX县某大型电器厂技术改造建建项目可行性研究方案.docx

-

安全生产责任清单.docx

-

毕业论文的引用7篇.docx

-

北体考研运动解剖名词解释概念.docx

-

北京市海淀区学年八年级下学期期末考试物理试题.docx

-

城镇道路工程施工与质量验收规范路基基层挡土墙.docx

-

春夜洛城闻笛教案.docx

-

初中学生期末报告册评语.docx

-

创卫工作总结例文三篇doc.docx

-

大海中的灯塔 大海上的灯塔叫什么.docx

-

参加文艺部竞选演讲稿.docx

-

大学实习生感谢信.docx

-

毕业生班级鉴定评语.docx

-

辞职信模板下载共8篇.docx

-

春节趣事作文500字合集九篇.docx

-

大学生养殖实践报告.docx

-

郴州妇女联合会.docx

-

python二级考试试题.docx

-

第7章截面几何性质答案.docx

不忘初心牢记使命我们的初心和使命优秀PPT党课课件+(含讲稿) (1)PPT课件下载推荐.ppt

不忘初心牢记使命我们的初心和使命优秀PPT党课课件+(含讲稿) (1)PPT课件下载推荐.ppt

- 版式设计 4、文字的魅力 版面文字设计1PPT文件格式下载.ppt

- 广告设计构图与版式设计PPT格式课件下载.ppt

- 学习习总书记关于金融工作的重要论述心得体会Word格式文档下载.docx

- 学习贯彻习近平总书记视察重庆重要讲话精神党课PPTPPT推荐.pptx

- 《不忘初心牢记使命》讲话精神学习解读PPT讲稿PPT课件下载推荐.ppt

- 版式设计图片与文字的编排2PPT资料.ppt

- 浅谈对习总书记“以人民为中心”思想的学习和理解文档格式.docx

- 内容水墨中国风习总书记的英雄情怀崇尚英雄主题PPT模板PPT格式课件下载.pptx

- 原创不忘初心牢记使命清正廉洁作表率党风廉政建设PPT微党课PPT文件格式下载.pptx