亨格瑞管理会计英文第15版练习答案05解读Word格式.doc

亨格瑞管理会计英文第15版练习答案05解读Word格式.doc

- 文档编号:13090157

- 上传时间:2022-10-04

- 格式:DOC

- 页数:45

- 大小:276KB

亨格瑞管理会计英文第15版练习答案05解读Word格式.doc

《亨格瑞管理会计英文第15版练习答案05解读Word格式.doc》由会员分享,可在线阅读,更多相关《亨格瑞管理会计英文第15版练习答案05解读Word格式.doc(45页珍藏版)》请在冰豆网上搜索。

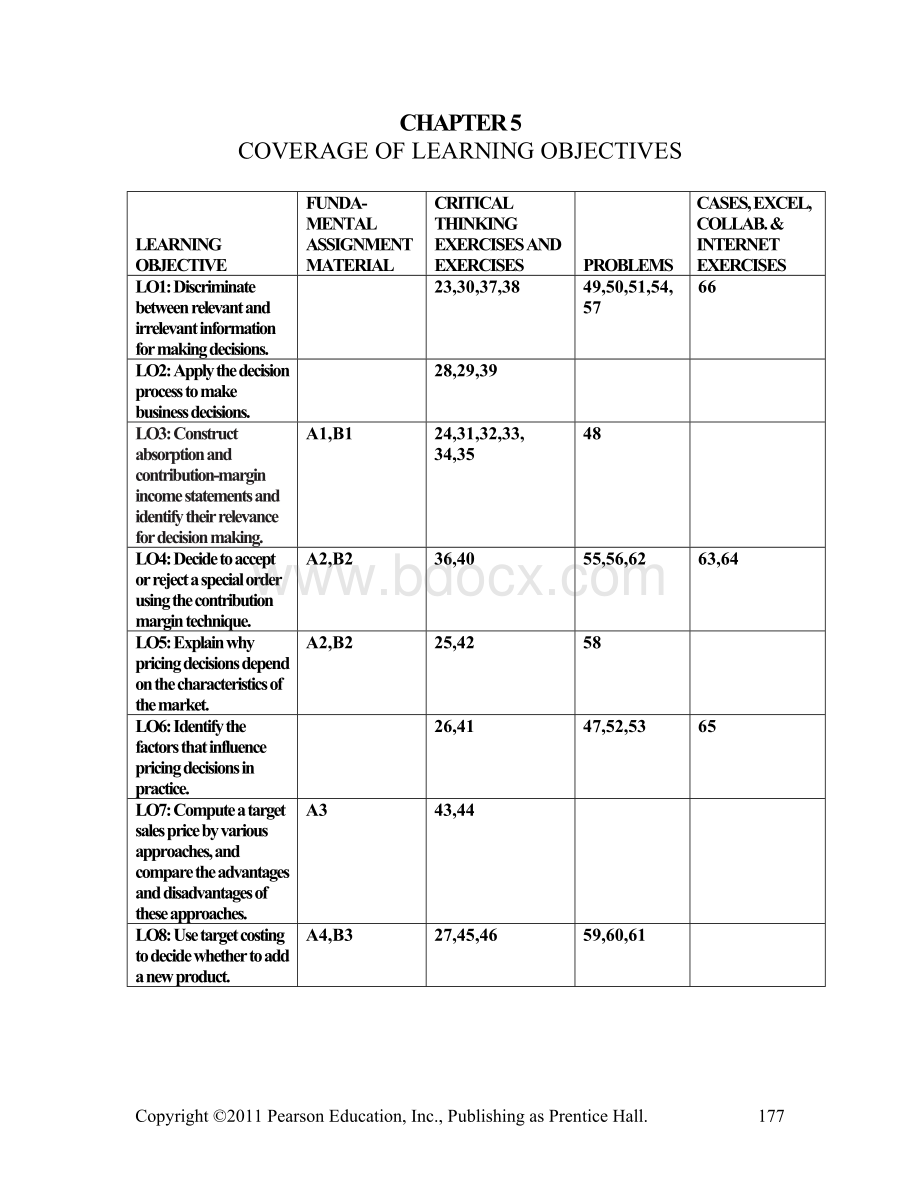

49,50,51,54,57

66

LO2:

Applythedecisionprocesstomakebusinessdecisions.

28,29,39

LO3:

Constructabsorptionandcontribution-marginincomestatementsandidentifytheirrelevance

fordecisionmaking.

A1,B1

24,31,32,33,34,35

48

LO4:

Decidetoacceptorrejectaspecialorderusingthecontributionmargintechnique.

A2,B2

36,40

55,56,62

63,64

LO5:

Explainwhypricingdecisionsdependonthecharacteristicsofthemarket.

25,42

58

LO6:

Identifythefactorsthatinfluencepricingdecisionsinpractice.

26,41

47,52,53

65

LO7:

Computeatargetsalespricebyvariousapproaches,andcomparetheadvantagesanddisadvantagesoftheseapproaches.

A3

43,44

LO8:

Usetargetcostingtodecidewhethertoaddanewproduct.

A4,B3

27,45,46

59,60,61

RelevantInformationforDecisionMakingwithaFocusonPricingDecisions

5-A1 (40-50min.)

1. INDEPENDENCECOMPANY

ContributionIncomeStatement

FortheYearEndedDecember31,2009

(inthousandsofdollars)

Sales $2,200

Lessvariableexpenses

Directmaterial $400

Directlabor 330

Variablemanufacturingoverhead(Schedule1) 150

Totalvariablemanufacturingcostof

goodssold $880

Variablesellingexpenses 80

Variableadministrativeexpenses 25

Totalvariableexpenses 985

Contributionmargin $1,215

Lessfixedexpenses:

Fixedmanufacturingoverhead(Schedule2) $345

Sellingexpenses 220

Administrativeexpenses 119

Totalfixedexpenses 684

Operatingincome $531

INDEPENDENCECOMPANY

AbsorptionIncomeStatement

FortheYearEndedDecember31,2009

Sales $2,200

Lessmanufacturingcostofgoodssold:

Manufacturingoverhead(Schedules1and2) 495

Totalmanufacturingcostofgoodssold 1,225

Grossmargin $975

Less:

Sellingexpenses $300

Administrativeexpenses 144 444

SchedulesofManufacturingOverhead

Schedule1:

VariableCosts

Supplies $20

Utilities,variableportion 40

Indirectlabor,variableportion 90 $150

Schedule2:

FixedCosts

Utilities,fixedportion $15

Indirectlabor,fixedportion 50

Depreciation 200

Propertytaxes 20

Supervisorysalaries 60 345

Totalmanufacturingoverhead $495

2. Changeinrevenue $200,000

Changeintotalcontributionmargin:

Contributionmarginratioinpart1

is$1,215÷

$2,200=.552

Ratiotimesdecreaseinrevenueis.552×

$200,000 $110,400

Operatingincomebeforechange 531,000

Newoperatingincome $420,600

Thisanalysisisreadilydonebyusingdatafromthecontributionincomestatement.Incontrast,thedataintheabsorptionincomestatementmustbeanalyzedandsplitintovariableandfixedcategoriesbeforetheeffectonoperatingincomecanbeestimated.

5-A2 (25-30min.)

1. Acontributionformat,whichissimilartoExhibit5-6,clarifiestheanalysis.

Without With

Special Effectof Special

Order SpecialOrder Order

Units 2,000,000 150,000 2,150,000

Total PerUnit

Sales $11,000,000 $660,000 $4.401 $11,660,000

Lessvariableexpenses:

Manufacturing $3,500,000 $322,500 $2.152 $3,822,500

Selling&

administrative 800,000 35,250 .2353 835,250

Totalvariableexpenses $4,300,000 $357,750 $2.385 $4,647,250

Contributionmargin $6,700,000 $302,250 $2.015 $7,002,250

Manufacturing $3,000,000 0 0.00 $3,000,000

administrative 2,200,000 0 0.00 2,200,000

Totalfixedexpenses $5,200,000 0 0.00 $5,200,000

Operatingincome $1,500,000 $302,250 $2.015 $1,802,250

1 $660,000÷

150,000=$4.40

2 Regularunitcost=$3,500,000÷

2,000,000= $1.75

Logo .40

Variablemanufacturingcosts $2.15

3 Regularunitcost=$800,000÷

2,000,000= $.40

Lesssalescommissionsnotpaid(3%of$5.50) (.165)

Regularunitcost,excludingsalescommission $.235

2. Operatingincomefromselling7.5%moreunitswouldincreaseby$302,250÷

$1,500,000=20.15%.Notealsothattheaveragesellingpriceonregularbusinesswas$5.50.Thefullcost,includingsellingandadministrativeexpenses,was$4.75.The$4.75,plusthe40¢

perlogo,lesssavingsincommissionsof.165¢

cameto$4.985.Thepresidentapparentlywanted$4.985+.08($4.985)=$4.985+.3988=$5.3838perpen.

Moststudentswillprobably

- 配套讲稿:

如PPT文件的首页显示word图标,表示该PPT已包含配套word讲稿。双击word图标可打开word文档。

- 特殊限制:

部分文档作品中含有的国旗、国徽等图片,仅作为作品整体效果示例展示,禁止商用。设计者仅对作品中独创性部分享有著作权。

- 关 键 词:

- 亨格瑞 管理 会计 英文 15 练习 答案 05 解读

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

第二章-传统相机的性能与种类.ppt

第二章-传统相机的性能与种类.ppt

三级健康管理师题库(附答案).docx

三级健康管理师题库(附答案).docx

-

房屋租赁合同范本(有法律效益).docx

-

合作协议书中(英文)版.docx

-

人音版小学三年级上册音乐教案.docx

-

餐饮店合股投资协议书.docx

-

城市综合管廊特点及设计要点解析.docx

-

机械助理工程师个人工作总结.docx

-

建设单位会议管理办法.docx

-

国有企业在“一带一路”中的发展路径.docx

-

幼儿园与家长签订的安全责任书.docx

-

2018年助理值班员职业技能竞赛专业知识考试试题及答案.docx

-

初中物理学科的核心素养.docx

-

军训结束教官讲话稿范本.docx

-

人教版新起点五年级英语上册全册教案.docx

-

唱歌跑调怎样办,唱歌超难听怎样办.docx

-

某拟提拔干部近三年工作总结.docx

-

最美教师事迹材料.docx

-

广播电视概论第一章绪论.pptx

-

质量管理体系考试试题及答案2.docx

-

《串联和并联》练习题.pptx

-

高端装备制造项目可行性研究报告.docx

-

新教师入职培训心得体会(9篇).docx

-

最新部编版三年级上册语文第8课《卖火柴的小女孩》教案第3单元教学设计.docx

-

2019年初级保育员理论知识考试真题及答案.docx

专业分包合同风险控制要点一览表 - 副本.rtf

专业分包合同风险控制要点一览表 - 副本.rtf

-

2019年最新主题教育围绕“四个对照”“四个找一找”在专题民主(组织)生活会个人对照检视检查研讨材料.docx

-

2018年度公司培训计划方案.docx

-

企业债券发行法律服务意向书---律所整理.docx

-

2019年事业单位法律知识考题及答案解析.docx

-

2019-2020学年人教版(新起点)英语五年级上册全册教案.docx

-

轨道焊接方案.docx

-

大学生小吃店创业计划书docx.docx

-

大自然的邮票.docx

-

飞度用户手册.docx

-

档案材料的基本装订要求.docx

-

风景区物业方案.docx

-

低保专项整治表态发言.docx

-

服装店劳动合同范本.docx

-

地理江苏省徐州市届高三下学期第一次质量检测地理试题+Word版含答案.docx

-

父母教养方式量表EMBU.docx

-

地质灾害应急对策及火灾应急对策.docx

-

干部档案审核标准和处理办法.docx

-

第三方服务合同.docx

-

第十三章突发公共卫生事件应对教案.docx

-

岗位分析及岗位说明书编写习题规程.docx

-

第一章运动休闲俱乐部概论.docx

-

高二升高三学生演讲稿.docx

-

电厂用水处理设备质量验收标准.docx

-

高考化学一轮复习 培优计划 第四章 非金属及化合物 二.docx

-

电话约人怎么才不被拒绝.docx