intermediate accountingfifteenth edition ch01.docx

intermediate accountingfifteenth edition ch01.docx

- 文档编号:10951555

- 上传时间:2023-02-23

- 格式:DOCX

- 页数:42

- 大小:44.37KB

intermediate accountingfifteenth edition ch01.docx

《intermediate accountingfifteenth edition ch01.docx》由会员分享,可在线阅读,更多相关《intermediate accountingfifteenth edition ch01.docx(42页珍藏版)》请在冰豆网上搜索。

intermediateaccountingfifteentheditionch01

CHAPTER1

FinancialAccountingandAccountingStandards

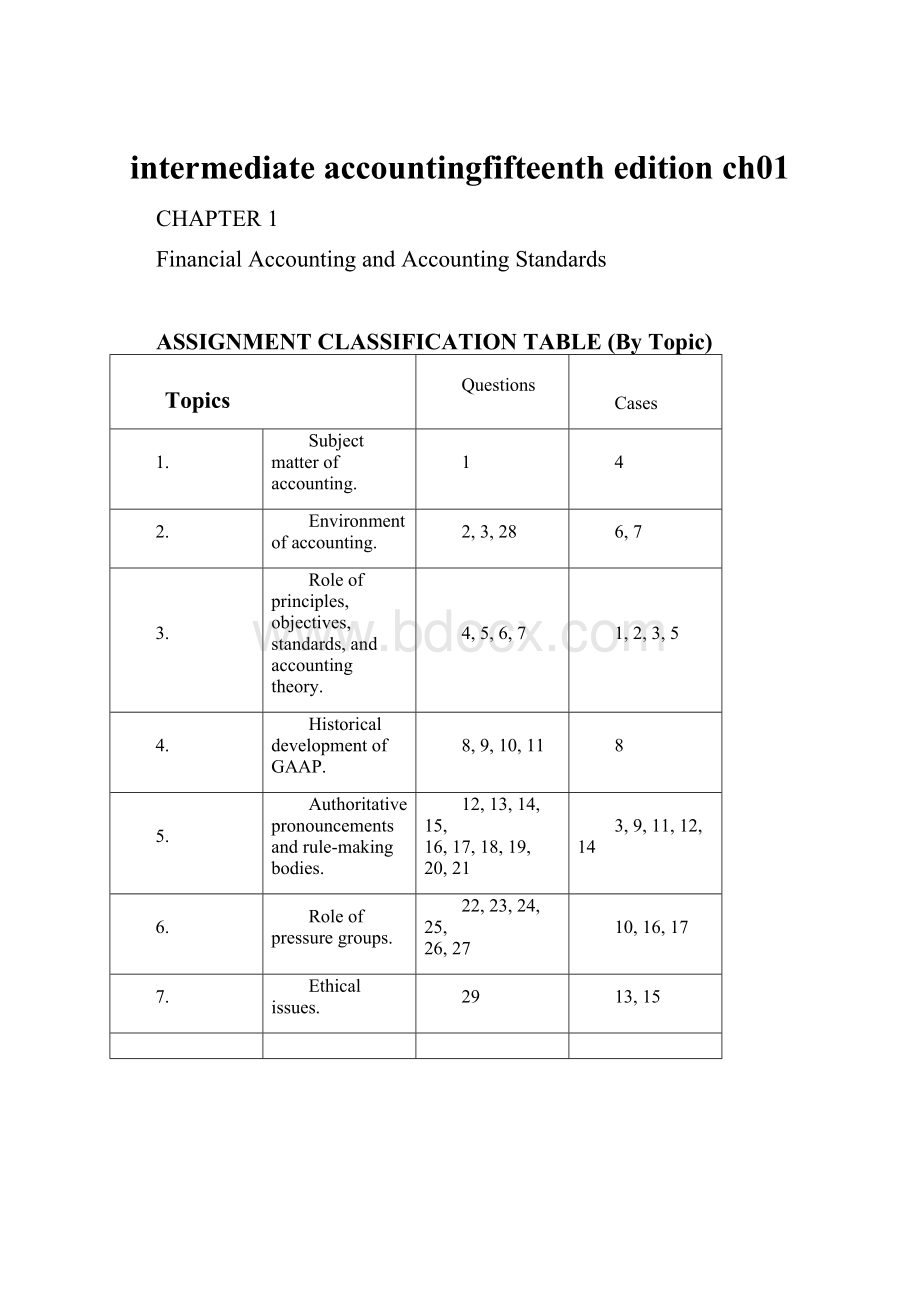

ASSIGNMENTCLASSIFICATIONTABLE(ByTopic)

Topics

Questions

Cases

1.

Subjectmatterofaccounting.

1

4

2.

Environmentofaccounting.

2,3,28

6,7

3.

Roleofprinciples,objectives,standards,andaccountingtheory.

4,5,6,7

1,2,3,5

4.

HistoricaldevelopmentofGAAP.

8,9,10,11

8

5.

Authoritativepronouncementsandrule-makingbodies.

12,13,14,15,

16,17,18,19,

20,21

3,9,11,12,14

6.

Roleofpressuregroups.

22,23,24,25,

26,27

10,16,17

7.

Ethicalissues.

29

13,15

ASSIGNMENTCLASSIFICATIONTABLE(ByLearningObjective)

LearningObjectives

Questions

Cases

1.

Identifythemajorfinancialstatementsandothermeansoffinancialreporting.

1,2

CA1-4,CA1-5

2.

Explainhowaccountingassistsintheefficientuseofscarceresources.

3,5

3.

Identifytheobjectiveoffinancialreporting.

4,7

CA1-2,CA1-3,CA1-4,CA1-5,CA1-6

4.

Explaintheneedforaccountingstandards.

6

CA1-3,CA1-7,CA1-9

5.

Identifythemajorpolicy-settingbodiesandtheirroleinthestandard-settingprocess.

8,9,10,11,13,14,15,16,19

CA1-1,CA1-2,CA1-3,CA1-7,CA1-8,CA1-9,CA1-11,CA1-14

6.

Explainthemeaningofgenerallyacceptedaccountingprinciples(GAAP)andtheroleofthecodificationforGAAP.

12,14,18,19,20,21

CA1-2,CA1-3,CA1-7,CA1-8,CA1-12

7.

Describetheimpactofusergroupsontherule-makingprocess.

17,22,23,24,25,26,27

CA1-10,CA1-11,CA1-13,CA1-16,CA1-17

8.

Describesomeofthechallengesfacingfinancialreporting.

28

9.

Understandissuesrelatedtoethicsandfinancialaccounting.

16,17,29

CA1-6,CA1-13,CA1-15

ASSIGNMENTCHARACTERISTICSTABLE

Item

Description

LevelofDifficulty

Time

(minutes)

CA1-1

FASBandstandard-setting.

Simple

15–20

CA1-2

GAAPandstandard-setting.

Simple

15–20

CA1-3

Financialreportingandaccountingstandards.

Simple

15–20

CA1-4

Financialaccounting.

Simple

15–20

CA1-5

Objectiveoffinancialreporting.

Moderate

20–25

CA1-6

Accountingnumbersandtheenvironment.

Simple

10–15

CA1-7

NeedforGAAP.

Simple

15–20

CA1-8

AICPA’sroleinrule-making.

Simple

20–25

CA1-9

FASBroleinrule-making.

Simple

20–25

CA1-10

PoliticalizationofGAAP.

Complex

30–40

CA1-11

ModelsforsettingGAAP.

Simple

15–20

CA1-12

GAAPterminology.

Moderate

30–40

CA1-13

Rule-makingIssues.

Complex

20–25

CA1-14

SecuritiesandExchangeCommission.

Moderate

30–40

CA1-15

Financialreportingpressures.

Moderate

25–35

CA1-16

Economicconsequences.

Moderate

25–35

CA1-17

GAAPandeconomicconsequences.

Moderate

25–35

SOLUTIONSTOCODIFICATIONEXERCISES

CE1-1

TheinformationatthislinkdescribestheelementsofferedinTheFASBAccountingStandardsCodification.Asindicated,thewebsiteoffersseveralresourcestoenhanceyourworkingknowledgeoftheCodificationandtheCodificationResearchSystem.ThispageincludeslinkstohelppageswhichdescribespecificfunctionsandfeaturesoftheCodification.Linkstofrequentlyaskedquestions,theFASBLearningGuide,andtheNoticetoConstituentsarealsoavailableonthispage.

Helppages

FAQ

LearningGuide

AbouttheCodification—NoticeofConstituents

CE1-2

ThefollowinginformationisprovidedattheProvidingFeedbacklink:

TheCodificationincludesafeaturewhichcanbeusedtosubmitcontent-relatedfeedbackorgeneral,system-relatedcomments.ThefeedbacksystemisnotdesignedforcommentsonproposedAccountingStandardsUpdates.

Content-relatedfeedback

AsaregistereduseroftheFASBAccountingStandardsCodificationResearchSystemwebsite,youareableandareencouragedtoprovidefeedback,attheparagraphlevel,totheFASBaboutanycontent-relatedmatters.ForspecificinformationabouttheCodificationandthefeedbackprocess,pleasereadtheNoticetoConstituents.

Toprovidecontent-relatedfeedback:

ClicktheSubmitfeedbackbuttonbeneaththeparagraphforwhichyouwanttoprovidefeedback.Enterorcopy/pasteyourcommentsinthetextbox.Notethatformatting(lists,bold,etc.)isnotretainedandthereisa4,000characterlimitonfeedbacksubmissions.

ClickSUBMIT.YourcommentsaresenttotheFASBandreviewedbyFASBstaff.Youcanalsosubmitmultiplecommentsforanygivenparagraph,if,forexample,youdeterminethatmoreinformationwouldbeusefultotheFASBstaff.

Generalfeedback

ClickheretoprovidegeneralfeedbackontheCodificationingeneral,theCodificationResearchSystemwebsite,andothersystem-relateditemsthatarenotcontentspecific.

CE1-3

The“What’sNew”pageprovideslinkstoCodificationcontentthathasbeenrecentlyissued.Duringtheverificationphase,updatesmayresultfromeithertheissuanceofCodificationupdateinstructionsthataccompanynewStandardsorfromchangestotheCodificationduetoincorporationofconstituentfeedback.

ANSWERSTOQUESTIONS

1.Financialaccountingmeasures,classifies,andsummarizesinreportformthoseactivitiesandthatinformationwhichrelatetotheenterpriseasawholeforusebypartiesbothinternalandexternaltoabusinessenterprise.Managerialaccountingalsomeasures,classifies,andsummarizesinreportformenterpriseactivities,butthecommunicationisfortheuseofinternal,managerialparties,andrelatesmoretosubsystemsoftheentity.Managerialaccountingismanagementdecisionorientedanddirectedmoretowardproductline,division,andprofitcenterreporting.

2.Financialstatementsgenerallyrefertothefourbasicfinancialstatements:

balancesheet,incomestatement,statementofcashflows,andstatementofchangesinowners’orstockholders’equity.Financialreportingisabroaderconcept;itincludesthebasicfinancialstatementsandanyothermeansofcommunicatingfinancialandeconomicdatatointerestedexternalparties.Examplesoffinancialreportingotherthanfinancialstatementsareannualreports,prospectuses,reportsfiledwiththegovernment,newsreleases,managementforecastsorplans,anddescriptionsofanenterprise’ssocialorenvironmentalimpact.

3.Ifacompany’sfinancialperformanceismeasuredaccurately,fairly,andonatimelybasis,therightmanagersandcompaniesareabletoattractinvestmentcapital.Toprovideunreliableandirrelevantinformationleadstopoorcapitalallocationwhichadverselyaffectsthesecuritiesmarket.

4.Theobjectiveofgeneralpurposefinancialreportingistoprovidefinancialinformationaboutthereportingentitythatisusefultopresentandpotentialequityinvestors,lenders,andothercreditorsindecisionsaboutprovidingresourcestotheentitythroughequityinvestmentsandloansorotherformsofcredit.Informationthatisdecision-usefultocapitalproviders(investors)mayalsobeusefultootherusersoffinancialreportingwhoarenotinvestors.

5.Investorsareinterestedinfinancialreportingbecauseitprovidesinformationthatisusefulformakingdecisions(referredtoasthedecision-usefulnessapproach).Whenmakingthesedecisions,investorsareinterestedinassessingthecompany’s

(1)abilitytogeneratenetcashinflowsand

(2)management’sabilitytoprotectandenhancethecapitalproviders’investments.Financialreportingshouldthereforehelpinvestorsassesstheamounts,timing,anduncertaintyofprospectivecashinflowsfromdividendsorinterest,andtheproceedsfromthesale,redemption,ormaturityofsecuritiesorloans.Inorderforinvestorstomaketheseassessments,theeconomicresourcesofanenterprise,theclaimstothoseresources,andthechangesinthemmustbeunderstood.

6.Acommonsetofstandardsappliedbyallbusinessesandentitiesprovidesfinancialstatementswhicharereasonablycomparable.Withoutacommonsetofstandards,eachenterprisecould,andwould,developitsowntheorystructureandsetofpractices,resultinginnoncomparabilityamongenterprises.

7.General-purposefinancialstatementsarenotlikelytosatisfythespecificneedsofallinterestedparties.Sincetheneedsofinterestedpartiessuchascreditors,managers,owners,governmentalagencies,andfinancialanalystsvaryconsiderably,itisunlikelythatonesetoffinancialstatementsisequallyappropriateforthesevarieduses.

QuestionsChapter1(Continued)

8.TheSEChasthepowertoprescribe,inwhateverdetailitdesires,theaccountingpracticesandprinciplestobeemployedbythecompaniesthatfallwithinitsjurisdiction.BecausetheSECreceivesauditedfinancialstatementsfromnearlyallcompaniesthatissuesecuritiestothepublicorarelistedonthestockexchanges,itisgreatlyinterestedinthecontent,accuracy,andcredibilityofthestatements.FormanyyearstheSECreliedontheAICPAtoregulatetheprofessionanddevelopandenforceaccountingprinciples.Lately,theSEChasassumedamoreactiveroleinthedevelop-mentofaccountingstandards,especiallyintheareaofdisclosurerequirements.InDecember1973,inASRNo.150,theSECsaidtheFASB’sstatementswouldbepresumedtocarrysubstantialauthoritativesupportandanythingcontrarytothemtolacksuchsupport.Ittherebysupportsthedevelopmentofaccountingprinciplesintheprivatesector.

9.TheCommitteeonAccountingProcedurewasaspecialcommitteeoftheAmericanInstituteofCPAsthat,betweentheyearsof1939and1959,issued51AccountingResearchBulletinsdealingwithawidevarietyoftimelyaccountingproblems.Thesebulletinsprovidedsolutionstoimmediateproblemsandnarrowedtherangeofalternativepractices.But,theCommittee’sproblem-by-problemapproachfailedtoprovideawell-definedand

- 配套讲稿:

如PPT文件的首页显示word图标,表示该PPT已包含配套word讲稿。双击word图标可打开word文档。

- 特殊限制:

部分文档作品中含有的国旗、国徽等图片,仅作为作品整体效果示例展示,禁止商用。设计者仅对作品中独创性部分享有著作权。

- 关 键 词:

- intermediate accountingfifteenth edition ch01

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

《JAVA编程基础》课程标准软件16级.docx

《JAVA编程基础》课程标准软件16级.docx

-

《分数的初步认识》.docx

-

《金属钠的性质与应用》教学设计.docx

-

《蚕妇》.docx

-

《会计》教材Word版第14章非货币性资产交换.docx

-

《与朱元思书》教学案例及反思.docx

-

《小壁虎借尾巴 》教案.docx

-

1第一部分 辅导员岗位基本知识.docx

-

09年CFO复习题.docx

-

2G1计算书.docx

-

17 古诗五首夜雨寄北一等奖教案.docx

-

240T15mw机组整体启动方案解析.docx

-

485总线设计方案加上位机扩展.docx

-

Aspose Word模板使用总结.docx

-

CDMA掉话分析.docx

-

C++新闻信息管理系统.docx

-

《HSE管理体系的策划与运行》.docx

-

c语言改错题及答案.docx

-

CMS7000使用说明资料.docx

-

《财经法规与会计职业道德》模拟卷考试试题及答案资料.docx

-

《大众传播媒介的更新》教案2.docx

-

《教育知识与能力》中学版全国教师资格考试复习资料教学教材.docx

-

EPC施工组织设计1.docx

-

ERP在服装行业的信息化应用可行性研究报告.docx

-

《项羽之死》教案人教版高二选修教学设计.docx

-

《公共关系实务》总复习资料.docx

-

FLUKE744过程校准仪经典实例免费给大家会让你未来的道路更通达.docx

-

《护士条例》试题.docx

-

2F男鞋统装规范84.docx

-

4测试用例修复方法与工具.docx

-

MC尼龙轮项目可行性研究报告.docx

-

Weblogic Server系统管理手册.docx

-

鞍山市部编人教版语文二年级下册全册知识点考点归纳整理大全.docx

-

初中毕业教师感言.docx

-

川大《公共关系学5003》20春在线作业10001参考答案.docx

-

版高考物理一轮复习第八章恒定电流第2讲电路的基本规律和应用学案.docx

-

办公室年终总结.docx

-

按11G1011图集钢筋工程量计算.docx

-

北京XX五金城专业市场招商手册23页DOCdoc.docx

-

保险专业代理机构办事.docx

-

北师大版一年级数学下册第五单元加与减二综合练习题106.docx

-

第三期师德大讲堂网络直播观后感心得最新5篇精选.docx

-

辨析病句的十个特殊标志词分析.docx

-

部编本二年级语文下册期末分类总复习题.docx

-

财政学第二版安秀梅讲义第六章 公共收入总论.docx

-

初中运动会广播稿精选.docx

-

单一来源采购文件范本.docx

-

Im watching TV上课学习上课学习教案1.docx

-

What time do you get up.docx

-

XX地区救护消防中队元旦春节应急救援预案.docx

-

XX一年级数学上第十单元20以内的进位加法教学设计苏教版.docx

链接地址:https://www.bdocx.com/doc/10951555.html